- Elliptic traced at least $507m in Tether USDT through about 50 wallets linked to Iran’s central bank, indicating trade and dollar access outside banks.

- Tether says it follows sanctions rules and has frozen $3.4bn with 310 agencies, while UK politics examine links involving Reform UK and USDT.

Iran’s central bank has become a focal point in a growing debate over cryptocurrencies, sanctions, and financial oversight, after new analysis suggested it has used large volumes of Tether’s USDT stablecoin to move value outside the traditional banking system. The revelation intersects with domestic repression in Iran, Western sanctions policy, and political advocacy for digital assets in the UK and US, raising questions about how a dollar-pegged token now sits at the centre of a sensitive geopolitical and regulatory dispute.

The rise of Tether and Iran’s central bank in a sanctions-driven crypto shift

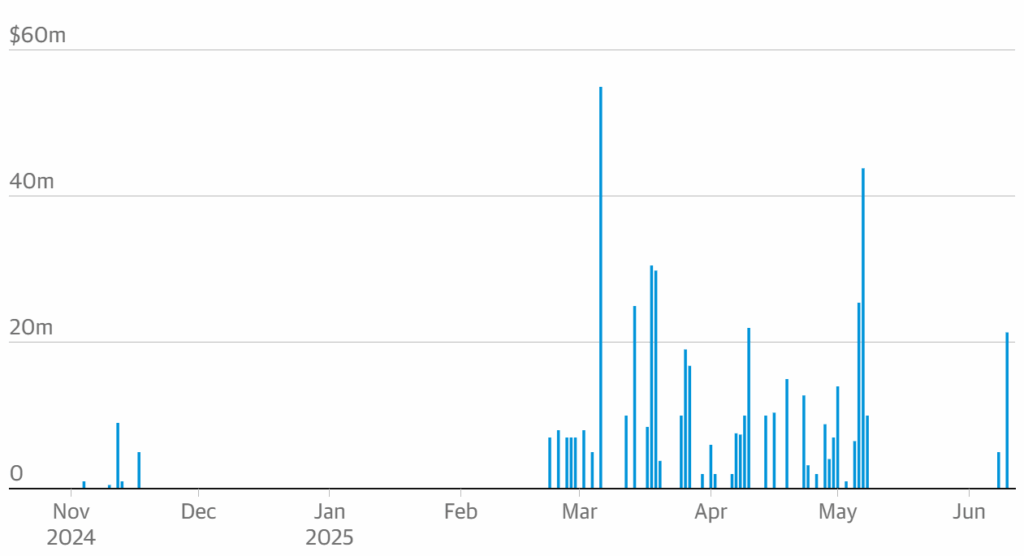

A recent report from blockchain analytics firm Elliptic traced at least $507 million worth of Tether’s USDT passing through accounts believed to belong to Iran’s central bank, indicating what the researchers described as a systematic build-up of stablecoins over time. The token, issued by Tether and pegged one-to-one to the US dollar, offers users in tightly controlled economies a liquid route into synthetic dollar exposure, which they can then convert into hard currency or use for cross-border trade that sidesteps conventional correspondent banking channels. According to Elliptic, transaction patterns around these accounts point to a deliberate, rather than incidental, strategy by Iran’s central bank to use USDT as an alternative rail, with flows spread across roughly 50 linked wallets that the firm associated with the institution with what it called a high level of confidence. The report suggested that this accumulation of Tether likely served multiple purposes for Iran’s central bank, which faces extensive US, UN and other international sanctions that restrict its access to global financial infrastructure and block large swathes of its activity from the mainstream dollar system. One likely use is trade settlement, where stablecoins can bridge gaps created by the exclusion of Iranian entities from many banks and payment networks, allowing them to pay for imports or receive proceeds from exports through intermediaries willing to accept crypto. Another potential use is support for the rial, Iran’s currency, which has suffered repeated bouts of devaluation; by holding and managing a stock of USDT, Iran’s central bank can access a pool of dollar-linked liquidity that can feed parallel markets and ease pressure on domestic foreign-exchange shortages without touching sanctioned banking corridors. Elliptic’s discovery did not come from an official disclosure by Iran’s central bank, but from an indirect trail: after Israel announced it had identified dozens of crypto accounts linked to Iran’s Revolutionary Guards last year, an Iranian businessman publicly complained on X that the authorities had failed to keep their dealings confidential. In that post, he included two wallet addresses that he said belonged to Iran’s central bank. Investigators at Elliptic followed the money moving through those wallets, mapped connections to other addresses, and eventually outlined a network that handled more than $500 million in USDT, with daily inflows shifting over time as sanctions, enforcement, and market conditions evolved.

Domestic repression and the use of USDT under sanctions

The growing use of USDT in Iran sits against a backdrop of severe domestic repression and widespread protests that followed high-profile abuses by the authorities, with thousands reported killed in crackdowns across the country. In this climate, the economic pressure on ordinary Iranians, combined with strict capital controls and sanctions that impede access to foreign currency, has led many individuals and businesses to seek alternative channels for trade and savings. Iran’s central bank, under pressure to manage inflation, currency volatility and external constraints, appears to have turned to the same tool that private users favour: stablecoins, with Tether’s USDT standing at the centre because of its dominant liquidity and acceptance on major exchanges. Sanctions limit Iran’s ability to hold accounts with many international banks, restrict dollar clearing, and complicate even basic trade finance, which in turn pushes actors inside the country toward instruments that can move across borders without traditional intermediaries. Iran’s central bank seems to have integrated USDT into this environment by orchestrating flows through crypto accounts that use the public blockchain for settlement but often rely on opaque intermediaries for off-ramp conversion. The Elliptic report described this pattern as a sophisticated attempt to bypass the global banking system rather than a scattered effort by smaller entities, and linked it to a broader shift in how sanctioned states use digital assets. The Iranian government has previously experimented with crypto-related strategies, including attempts to encourage domestic Bitcoin mining in order to turn subsidised electricity into exportable value. The apparent use of USDT by Iran’s central bank goes a step further by tying state-level monetary and trade operations directly to a private stablecoin issuer that holds real-currency reserves outside Iran’s jurisdiction. This approach carries both advantages and risks. On one side, it allows sanctioned institutions to move value with fewer chokepoints. On the other, it exposes them to the policies and compliance decisions of Tether and the exchanges and over-the-counter desks that handle conversion, any of which can freeze assets or cut off access in response to law enforcement and regulatory pressure.

Political fallout, Nigel Farage, and the defence of Tether amid Iran’s central bank links

The alleged use of USDT by Iran’s central bank has resonated beyond Iran’s borders because of the political and financial interests tied to Tether in Western countries. In the UK, Nigel Farage, leader of Reform UK, has become an outspoken supporter of stablecoins, singling out Tether as an example of innovation he believes the country should embrace. In September, he said in a radio interview that he planned to raise Tether with Bank of England governor Andrew Bailey, arguing that stablecoins act as the bridge between conventional currencies and the wider crypto market, and predicting that Tether would soon have a valuation of around $500 billion. He criticised Bailey for imposing restrictions that, in his view, put the UK behind the United States, where he pointed to former president Donald Trump’s more permissive stance on digital assets and highlighted Trump’s selection of Howard Lutnick, a Tether banking partner, as commerce secretary. These comments now sit uneasily alongside reports that Iran’s central bank has used the same stablecoin that Farage has praised, particularly given the regime’s record on human rights and the harsh suppression of protests. Critics argue that promoting an asset so heavily used in sanctioned environments risks undermining broader foreign-policy goals. Supporters counter that the responsibility lies with enforcement mechanisms and that the underlying technology remains neutral. Reform UK has responded to the Elliptic findings by stressing that many companies and organisations around the world use Tether, stating that all donations to the party comply with electoral law and that each contribution goes through a vetting process. The party has also said it continues to support the Iranian people in their struggle for freedom, drawing a distinction between regime use of financial tools and solidarity with protesters. Funding ties add another layer to the controversy. Christopher Harborne, a tech investor and one of Tether’s major shareholders, is the largest donor to Reform UK. His lawyers have said that he does not hold an executive role at Tether and therefore cannot bear responsibility for illicit actions by users of the stablecoin, dismissing suggestions that he profits directly from Iran’s central bank use of USDT as baseless. This defence goes to the heart of a wider policy question: how far responsibility travels along the chain from issuer to shareholder to political recipient when a digital asset becomes embedded in sanctioned financial activity and in the operations of institutions such as Iran’s central bank.

Tether’s compliance stance, enforcement record and outlook

Tether, for its part, has emphasised its compliance and enforcement efforts without directly addressing the specific claim that Iran’s central bank uses its stablecoin at scale. A company representative has said that Tether operates with a zero-tolerance policy toward criminal activity involving its products and that it follows US sanctions guidelines in its monitoring and response processes. According to Tether, it has worked with more than 310 law enforcement agencies in 62 countries and has frozen over $3.4 billion in assets tied to criminal activity, highlighting a record that the firm argues shows a willingness to cooperate when authorities identify illicit flows. Following public disclosures by Israel about crypto accounts used by Iran’s Revolutionary Guards, Tether froze the wallets that Israel had flagged, cutting off those specific channels. However, the accounts that Elliptic associated with Iran’s central bank mostly remain active, according to the analytics firm’s report, indicating that no broad freeze has occurred on that cluster. This difference illustrates a key tension in Tether’s position: it aims to follow formal sanctions guidance and respond to concrete law-enforcement requests, while not acting as a unilateral arbiter of which state-linked accounts can or cannot use USDT, especially when those accounts sit in a grey zone between formal designation and suspicion based on analytic inference. Behind this dispute lies Tether’s immense profitability and global reach, which give the company both resources and influence. Demand for USDT has helped Tether generate annual profits estimated at around $13 billion, roughly one and a half times the earnings of McDonald’s, driven in large part by the yield on the reserves it holds to back its tokens. A share of that demand comes from regions where access to reliable fiat currency is constrained, whether by inflation, capital controls, or sanctions. Iran’s central bank appears to have tapped into this supply of digital dollars precisely because it offers a pragmatic workaround to the hard limits imposed on its participation in conventional finance. As more jurisdictions scrutinise stablecoins and as analytics firms continue to map flows associated with sanctioned actors, Tether and institutions such as Iran’s central bank will face growing pressure over how these tokens function in practice within a contested and fragmented global system.

Conclusion

The emerging picture of Iran’s central bank using large volumes of Tether’s USDT reveals how a private stablecoin has become a practical tool for a heavily sanctioned institution seeking access to dollar-linked liquidity outside normal banking channels. Elliptic’s tracing of more than $507 million in flows across about 50 wallets, the public fall-out from Israel’s exposure of Revolutionary Guards accounts, and the political scrutiny now touching supporters of Tether in the UK all underscore the complex role that digital assets play at the intersection of monetary policy, sanctions enforcement and human rights concerns. As Tether highlights billions of dollars in frozen assets and cooperation with hundreds of law enforcement agencies, and as Iran’s central bank continues to navigate sanctions and domestic pressure, the debate over stablecoins and their place in the global financial order will intensify, with each new disclosure adding to the questions around transparency, accountability and the limits of control in an open blockchain environment.

Disclaimer

The information provided in this article is for informational purposes only and should not be considered financial advice. The article does not offer sufficient information to make investment decisions, nor does it constitute an offer, recommendation, or solicitation to buy or sell any financial instrument. The content is opinion of the author and does not reflect any view or suggestion or any kind of advise from CryptoNewsBytes.com. The author declares he does not hold any of the above mentioned tokens or received any incentive from any company.

Featured image created by AI

Subscribe To Our Newsletter

Join our mailing list to receive the latest news and updates from our team.