- China begins paying demand deposit style interest on verified digital yuan wallets from 2026, moving the CBDC closer to deposit money than simple digital cash.

- The policy brings e CNY under deposit insurance within existing bank structures, creating practical questions for banks, regulators and other CBDC projects.

China’s central bank digital currency entered a new phase on 1 January 2026. On that date, digital yuan wallets started to earn interest at standard demand deposit rates. The shift turned what had once been treated as pure digital cash into something closer to a bank account. This quiet switch in China pushed the project beyond the testbed stage and into a new policy experiment that challenges years of guidance from global institutions. Many of those institutions wanted central bank digital currencies, or CBDCs, to remain non-interest-bearing. At the same time the change signalled that the authorities now see the digital yuan not only as a payment instrument but also as a tool for bank funding, monetary policy transmission and competition with private payment platforms. Behind the technical change lies a clear political and economic decision by China to depart from the template that the European Central Bank, the Federal Reserve and the Bank for International Settlements have promoted. In that template a digital euro or digital dollar would work like cash and never pay interest. Instead of following this model, Beijing has chosen to blur the line between digital notes in circulation and sight deposits while still insisting that the move will not drain liquidity from commercial banks.

China redefines the role of retail CBDC with interest bearing e CNY

When the new rules took effect, verified digital yuan wallets in categories one to three began to accrue interest calculated under the same rules that apply to ordinary demand deposits. Settlement takes place on the twentieth day of the final month of each quarter. Anonymous wallets in the fourth category, which have stricter balance and usage limits, remain outside the interest regime. That split keeps a gap between fully identified users and small, lightly vetted accounts. The People’s Bank of China placed these changes inside an “Action Plan for Strengthening Digital Yuan Management and Financial Infrastructure,” a document that anchors the currency more firmly inside the traditional banking system by allowing balances in commercial bank wallets to count as deposit liabilities on bank balance sheets. By November 2025, users in China had opened around 230 million digital yuan wallets and processed cumulative transactions of 16.7 trillion yuan across domestic pilots. These figures already made the project the world’s largest retail CBDC trial even before the interest flip. They also help explain why the authorities in China decided to strengthen the link between the digital currency and regular deposit accounts. A system of that size can no longer sit at the edge of the banking sector. At the same time the interest feature creates a modest financial reason to hold balances instead of moving funds out immediately after each payment, which may reduce the dominance of private super-apps that had long set the pace in China’s mobile payments market. The central bank also confirmed that funds held in compliant digital yuan wallets would fall under the country’s deposit insurance scheme. That means these balances carry the same formal protection as money in ordinary current accounts. The decision tries to resolve one of the dilemmas in CBDC design, because insured and interest-bearing central bank money can look safer than commercial bank deposits during periods of stress. Policymakers in China believe that the two-tier structure of the system, in which commercial banks and payment institutions still provide the interface to end users, will keep the traditional institutions at the centre of daily financial life even as the role of public money grows.

Global orthodoxy on CBDC design and how China breaks it

For more than a decade, central banks and international bodies sketched out a cautious model for retail CBDCs that placed stability above innovation. The ECB’s technical work on a future digital euro states in plain terms that balances would not receive interest. It also notes that design choices such as holding limits should prevent the new instrument from competing with bank deposits as a store of value. The Federal Reserve’s 2022 discussion paper on a potential digital dollar expressed similar worries. That paper warned that an interest-bearing CBDC could change the structure of the financial system by drawing funds away from banks, raising their funding costs and reducing their ability to extend credit to households and firms. For China and for other large economies, research by the BIS and the IMF has reinforced these themes. Those studies highlight the risk that, during a crisis, households might rush out of private bank deposits into central bank wallets if those wallets paid interest and offered a direct claim on the state. Under that view, CBDCs should behave like digital banknotes rather than interest-bearing accounts. The policy compromise that emerged in many advanced economies involves non-interest-bearing balances, tight caps on individual holdings and tiered privacy rules that offer some anonymity for low-value payments while reserving full identification for higher-value use. China’s choice to pay interest, while also classifying many digital yuan balances as bank deposits, sits uneasily inside that framework. It effectively transforms part of the money supply that once counted as M0, or cash in circulation, into something closer to M1. In that broader measure, statisticians bundle current accounts and other instantly available deposits. The action plan also updates the definition of the currency itself to cover not only the digital tokens but also the associated payment infrastructure. That wording change hints at a broader ambition to use the system as a common layer for programmable payments and contracts rather than just a series of isolated wallets. Academic work has started to chip away at the zero-interest orthodoxy that dominated early CBDC debates and influenced thinking in China as well. A 2025 analysis published through the CEPR looked at a model where banks face competition from a central bank currency. In that setting welfare improves when the CBDC rate either stays at zero or sits roughly one percentage point below the prevailing policy rate, whichever is higher. The study suggests that moderate interest on central bank money can weaken the market power of banks without destroying their role in credit intermediation. This line of reasoning aligns more closely with the direction that officials in China have now taken.

China, digital yuan architecture and the shift from M0 to M1

The technical structure of the e-CNY in China aims to soften the impact of the new interest feature on commercial banks while still moving the project into the core of the financial system. Under the two-tier model, the central bank issues digital yuan to a set of operating institutions, mainly large banks and regulated payment firms. Those firms in turn distribute and manage wallets for the public and for businesses. That arrangement keeps familiar intermediaries in front of users, even though the underlying liability remains a claim on the central bank. It also lets regulators adjust requirements for different wallet tiers through familiar prudential tools. By allowing balances in many of these wallets to count as deposit liabilities, the authorities in China give banks a reason to treat the digital currency as part of their funding base rather than as a threat. Interest paid on wallets will follow deposit-rate rules, which remain under the influence of the central bank’s broader policy stance and existing guidance on pricing. That link gives monetary policy a more direct route into the pockets of households, because changes in official rates can flow into digital yuan holdings without waiting for banks to adjust loan and deposit terms on their own schedules. Mobile payments in China already operate at large scale through private platforms, and the digital yuan competes for user attention in that environment. By the end of 2025, cumulative e-CNY transactions in China had reached 16.7 trillion yuan in trial regions. That figure reflects real usage but still sits below the volumes handled by Alipay and WeChat Pay. Adding interest creates a new incremental reason to keep some balance on the state-backed platform, especially for users who already rely on mobile apps for day-to-day spending. It also embeds the central bank more firmly in a data-rich segment of the payments market, which could prove useful for supervision, compliance and cross-border projects in the future. Domestic politics in China and the structure of its banking sector also shape why the authorities feel comfortable moving ahead where others hesitate. The banking system remains dominated by large state-linked groups, which stand to gain from deposit classification of digital yuan balances and from their position as key operating institutions for the project. Deposit insurance coverage, combined with tight controls on capital flows and a strong role for public entities, reduces the risk of sudden destabilising shifts in funding between banks and the central bank. In that setting, an interest-bearing CBDC looks less like a disruptive new competitor and more like an extension of the existing architecture of public finance.

How China’s move reshapes the global CBDC race and leaves the US on the sidelines

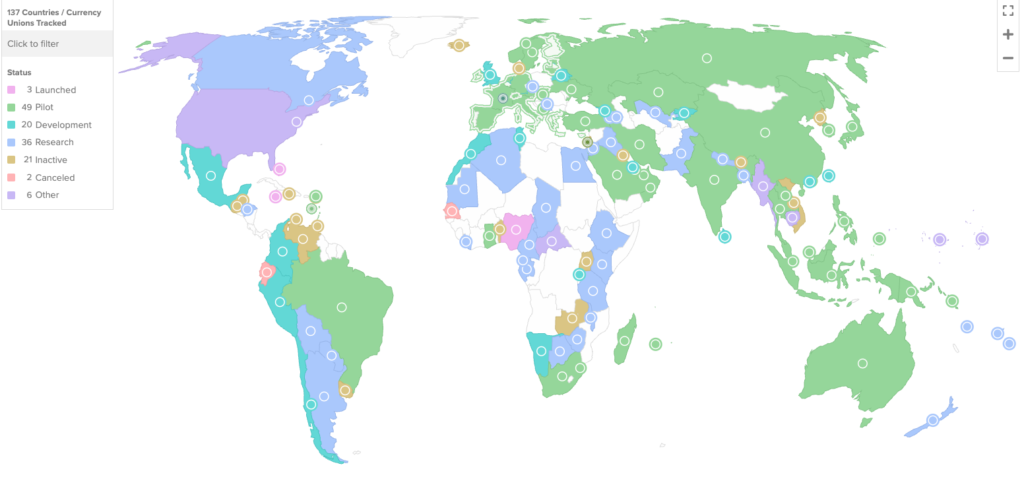

The decision in China to pay interest on the digital yuan lands at a moment when most major economies are still refining their own CBDC plans. Across the world, about 137 countries and currency unions, representing roughly 98% of global GDP, now explore some form of central bank digital currency. Many of them have moved beyond research into development or pilot stages. Within that group, China already operated the largest retail pilot even before the new action plan, while the euro area and India advanced their own projects with different priorities and constraints. European authorities continue to frame the digital euro as a payment instrument that should not compete with deposit products offered by banks. Public documents from the ECB and national central banks repeat that a digital euro would not pay interest and would likely include strict holding limits for individuals. Technical tools would convert balances above the ceiling back into commercial bank money. The stated goal is to preserve financial stability by stopping large-scale shifts from private deposits into direct claims on the central bank, even during periods of stress when such a shift might look attractive to households. The United States has taken a very different path from China. Early in 2025, President Donald Trump signed an executive order that barred federal agencies from developing, issuing or promoting a retail digital dollar, citing concerns about state overreach and privacy. Later that year, Congress passed a package of crypto-related laws during a period that became known as Crypto Week. That package included the GENIUS Act for stablecoins and a market-structure bill, as well as legislation designed to prevent the Federal Reserve from launching a CBDC. The anti-CBDC act still awaits final resolution in the Senate, but the combined effect of these steps has left the country as the only major jurisdiction with a formal political ban on a retail central bank digital currency. That choice has consequences for the balance of influence between China, Europe and a long list of emerging markets. With the United States on the sidelines, experiments in China and in the euro area will shape the technical standards, privacy frameworks and cross-border settlement models that smaller countries may adopt. European projects such as the digital euro and initiatives under the BIS Innovation Hub tend to stress privacy, limits and offline functionality. The approach in China connects the new money more tightly to existing bank accounts and transaction data. Other central banks now watch to see whether the interest-bearing model boosts usage of the digital yuan without putting undue pressure on bank funding or sparking volatility in deposit flows. For countries still designing their own CBDCs, the debate is no longer a simple question of whether to issue a digital version of national money. They must decide whether to align more with the cautious European template, the more deposit-like design that China now tests, or the hands-off approach that leaves private stablecoins and payment platforms to handle most innovation. Their choices will affect how easily people move value across borders, how monetary policy reaches households and how much transaction data sits in public hands rather than in private platforms.

Conclusion

The introduction of interest on digital yuan wallets marks a turning point for both China and the wider conversation about central bank digital currencies. A project that once looked like a pure cash substitute now operates much closer to a deposit system. Balances earn returns, enjoy deposit insurance and sit on bank balance sheets, yet still represent a claim on the central bank. That combination challenges the long-standing view that CBDCs should mimic physical notes and avoid any features that might encourage people to shift funds away from commercial banks. Other jurisdictions now face a more complex comparison that increasingly centres on China’s example. The euro area moves towards a digital euro that will not pay interest and will carry strict limits on individual holdings, while the United States steps back from retail CBDCs altogether and focuses on rules for stablecoins and other crypto assets. As more than one hundred countries continue their own experiments, they will watch closely whether the interest-bearing model in China enhances adoption without undermining financial stability or credit creation. The result will shape not only the future of the digital yuan but also the emerging global map of public digital money.

Disclaimer

The information provided in this article is for informational purposes only and should not be considered financial advice. The article does not offer sufficient information to make investment decisions, nor does it constitute an offer, recommendation, or solicitation to buy or sell any financial instrument. The content is opinion of the author and does not reflect any view or suggestion or any kind of advise from CryptoNewsBytes.com. The author declares he does not hold any of the above mentioned tokens or received any incentive from any company.

Featured image created by AI

Subscribe To Our Newsletter

Join our mailing list to receive the latest news and updates from our team.