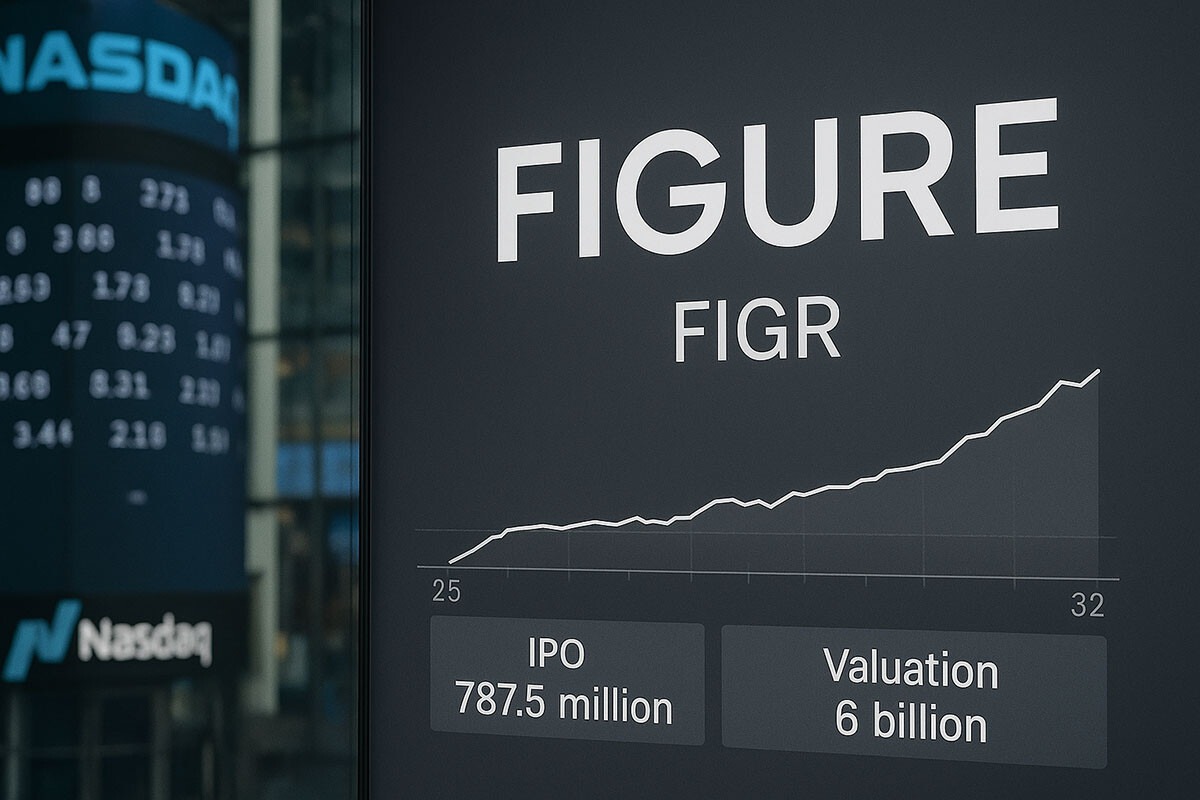

- Figure opened at $25 and reached $32 on first trading day

- IPO raised $787.5 million with market cap near $6 billion

- January to June revenue was $190 million with $30 million profit

The market watched figure make its public debut on Nasdaq after raising $787.5 million, opening at $25 per share and climbing almost 30% to about $32 by Thursday afternoon, which set an equity value near $6 billion for the ticker FIGR and shifted attention to how the company turns mortgages into blockchain-native assets and how that pipeline might scale.

figure IPO on Nasdaq: pricing, first-day action, valuation

Investors saw a straightforward setup at the open. The offering brought in $787.5 million in gross proceeds and set an initial list price of $25 per share. Trading pushed the stock to roughly $32 during the first session, a move of almost 30% that placed the post-IPO market capitalization around $6 billion. The result signaled interest in a company that ties consumer credit to blockchain rails and prefers to describe its listing as one step in a larger capital markets transition rather than a finish line. Mike Cagney, the cofounder and CEO, wrote to investors that the public listing forms part of a longer plan to bring distributed infrastructure into routine issuance, funding, and settlement. The first day did not settle every question about margins or funding costs, yet it created an observable price, a deeper float, and a reference point for future secondary offerings or acquisitions. Traders now have a clean view of FIGR’s sensitivity to rates, origination volumes, and secondary loan sales across quarters rather than anecdotes from private rounds.

figure business model: mortgages on blockchain and growth metrics

The core pitch remains simple to explain and complex to execute. figure originates and processes home loans, then records and manages assets on blockchain infrastructure to compress funding timelines and reduce operational friction. The company points to throughput as proof the workflow functions at scale. From June 2024 to June 2025, it facilitated about $6 billion in loans according to filings, which helps tie product talk to audited volume. From January through June 2025, it generated more than $190 million in revenue and nearly $30 million in net income, numbers that give analysts enough data to build basic run-rate models and stress test rate scenarios. If funding spreads stay stable, efficiency gains from standardized smart-contract tooling may lift operating margins. If spreads widen, the automation still matters, but investors will watch how quickly the company can cycle loans and at what discount in the secondary market. The thesis hinges on whether tokenized loan registries make custodial handoffs faster and cheaper without breaking compliance. That is not a marketing line; it is an execution checklist measured in closing times, warehouse costs, and error rates. The filings suggest measurable speedups in granting and funding, and the next quarters will show if those advantages persist when origination volumes rise or when rates move.

Crypto IPO context: Circle, Bullish, Gemini, Grayscale, Kraken

The listing landed in a busy calendar for digital-asset firms. In June, Circle completed a large IPO that raised more than $1 billion and briefly carried a market cap near $80 billion before falling toward about $30 billion later that month, showing how wide valuation bands can be in this segment even when revenue visibility looks stable. In August, exchange operator Bullish, led by former NYSE president Tom Farley, went public and now sits around an $8.5 billion market value, giving the market another liquid benchmark for crypto-linked order flow and fee capture. The pipeline remains active. Gemini has scheduled a Nasdaq listing for Friday, which adds a regulated exchange narrative with a distinct custody and compliance focus. Grayscale confidentially filed in July, which points to a potential conversion of brand equity in the ETF arena into public-market capital formation. Kraken continues to evaluate timing for a float, as reported over multiple cycles, and will likely weigh fee trends, enforcement outcomes, and cross-jurisdiction licensing before it finalizes a path. Against that backdrop, figure reads less like an outlier and more like a specialized credit platform using blockchain for asset plumbing rather than a pure trading venue. That distinction matters for index inclusion screens, coverage models, and multiples, since origination platforms track housing and credit cycles while exchanges track volatility and volume.

Mike Cagney, SoFi past and culture reset at figure

Public investors also price leadership track records, and this story carries a visible one. Mike Cagney previously cofounded SoFi, which later went public in 2021 through a separate route. He left SoFi in 2017 following a sexual harassment scandal that drove governance changes and executive turnover. In 2024, during a Fortune event, he acknowledged those issues and emphasized that he built figure with a stronger culture emphasis from the start. The framing matters because governance and culture affect execution in regulated finance, where a weak process can undo years of product work in a single compliance event. The pledge to treat figure as a more mature enterprise sets a bar that investors can test by watching hiring patterns, risk controls, and board oversight disclosures across upcoming filings. A market listing does not erase the past, but it does create recurring disclosure, which gives the public a way to evaluate whether promised culture standards show up in practice. If the company continues to meet revenue and net income targets while avoiding control failures, the leadership narrative may recast from controversy to operational delivery. If missteps recur, multiples will compress quickly, because financial firms trade on trust and process discipline as much as they trade on growth.

figure outlook: funding costs, loan velocity, and public-market signals

The near-term setup focuses on three levers that sit inside the business and one that sits outside. First, loan velocity will show whether blockchain-based registries truly shorten dwell time between origination and funding. Faster turns lower warehouse costs and can support higher volumes without linear cost growth. Second, net interest and fee dynamics will reveal how figure balances pricing with borrower demand in a rate environment that may shift quarter to quarter. Third, operating expense discipline will indicate whether automation offsets the headcount and vendor spend that usually grows with scale. The fourth lever remains exogenous: equity market risk appetite. Circle’s valuation arc, moving from a near $80 billion peak to about $30 billion within weeks, illustrates how quickly comps can swing and how sensitive crypto-linked equities remain to flows and narratives. Bullish at roughly $8.5 billion adds a separate comparator for exchange economics, while Gemini’s debut date gives another read on investor demand for compliant venues. Within that landscape, figure sits in the mortgage and credit lane with a blockchain backbone, so its comps may tilt toward fintech lenders rather than pure trading platforms. The company’s first half showing of more than $190 million in revenue and almost $30 million in net income establishes a baseline that modelers can carry into forecasts, but the market will want several quarters of public reporting to decide if those prints represent a steady state or a rate-driven spike. If the team keeps execution tight and avoids governance noise, the initial $6 billion valuation may track with fundamentals; if volumes or controls slip, the market will reset the multiple.

Conclusion

The debut put figure on a public scorecard with $787.5 million raised, an open at $25, a first-day push toward $32, and a market cap close to $6 billion, while filings show about $6 billion in loans over the year through June and more than $190 million in first-half revenue with almost $30 million in net income, leaving the next quarters to test whether blockchain-based loan workflows keep moving capital faster, whether operating discipline holds, and whether leadership delivers the culture it promised under public scrutiny.

Disclaimer

The information provided in this article is for informational purposes only and should not be considered financial advice. The article does not offer sufficient information to make investment decisions, nor does it constitute an offer, recommendation, or solicitation to buy or sell any financial instrument. The content is opinion of the author and does not reflect any view or suggestion or any kind of advise from CryptoNewsBytes.com. The author declares he does not hold any of the above mentioned tokens or received any incentive from any company.

Featured image created by AI