In the cutting-edge era of digitalization, crypto, and blockchain have emerged as a dramatic change in the fintech world and have reshaped people’s ideas. In a short time, the futuristic niche has gained much popularity worldwide and grabbed the attention of leading bankers. Recently according to a report, in June Goldman Sachs filed a patent application. According to the brief details, Goldman aims to support fractional banking for cryptocurrencies on distributed ledgers (DLTs).

Fractional banking is a relatively newer idea in the world of crypto. Many platforms were practicing the idea of fractional banking before. But at a larger scale, investors were reluctant to adopt this strategy formally, mainly due to the unpredictable nature of cryptocurrency.

The risky move of Goldsmith will possibly help to bridge the gaps between traditional and fractional banking. Moreover, it will also bring an era of digital contractors and efficient lending and browning channels to the crypto world. Join me as we explore the exciting possibilities and challenges of fractional banking on distributed ledgers in the crypto and blockchain.

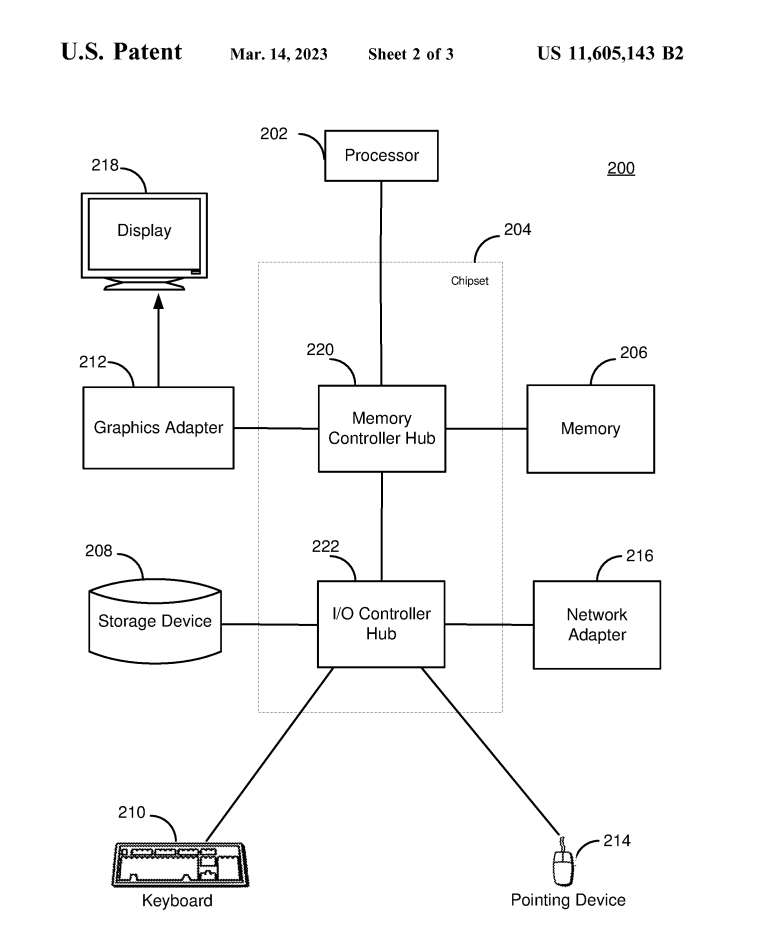

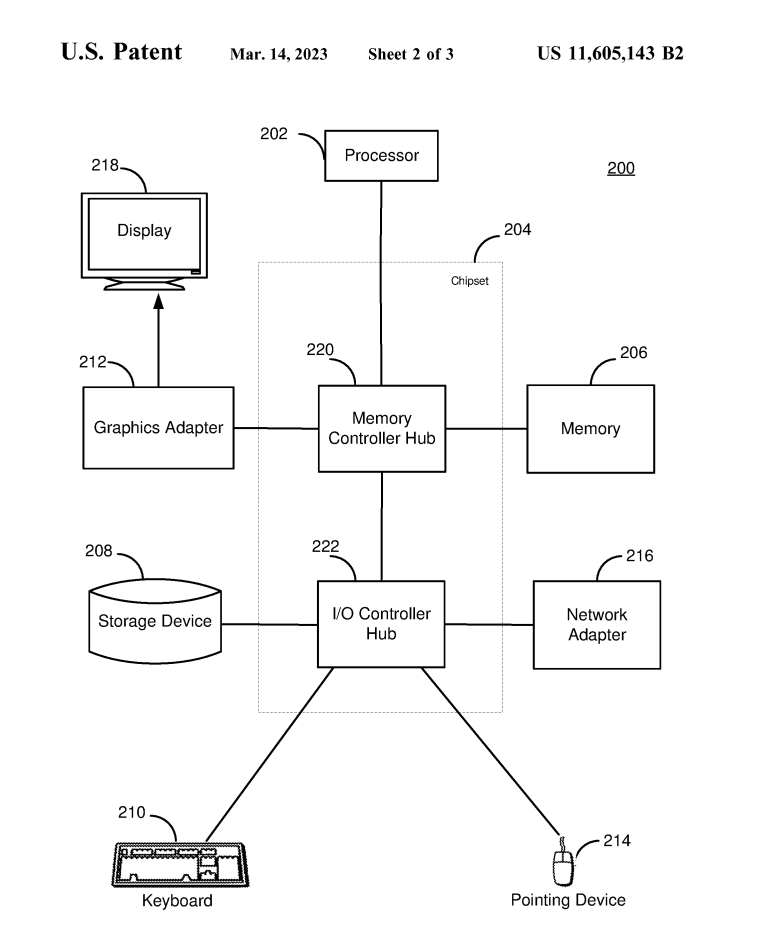

An Overview of Goldman’s Patent Application:

Here is what Goldman’s patent application, patent no: US 11, 605, 143 2B, discusses:

DLTs as the middleman: Analysis of the trends tells that many bankers may be reluctant to contribute towards fractional banking in crypto for that reason, Goldman proposed the use of Distributed ledgers. For my readers, you can call DLT a type of blockchain.

The decentralized nature of the database system will ensure transparency and efficiency through the use of smart contractors. These contractors will be automated and will take place as soon as the prerequisites are complete.

Fractional Reserves Tokens: Fractionally reserved tokens will be used to claim correspondent assets. For example, the system will generate a token for a pool of Bitcoins or Ethereum. Based on these tokens loans will be provided. A person can use cryptocurrency, real estate assets, government bonds, jewelry, or other commodities and bank deposits for fractional reserve tokens.

Scalable: Goldman will ensure the scalability and efficiency of the system through different trials before implication. It will be to ensure the system can accommodate a bigger user pool.

Risk Management: The risk management techniques are yet not revealed by Goldman. But surely they will be an important part of the idea. According to the anticipations, the risk management system will accommodate reserve requirements, collateral requirements such as real estate and other commodities, liquidity management, and cyber security.

Future and Challenges for Goldman’s Innovative Idea:

The future of fractional banking in the crypto sector is uncertain. We can expect a promising future and a complete flop. Here are the factors that will contribute to a prospective future:

Wide Liquidity: Fractional banking will act as a gateway for the wider availability of cryptocurrency. This is because people could easily trade their currencies. This aspect may also be beneficial in controlling the volatility of the cryptocurrency.

Efficient Financial System: If the system is successful, it can cut off the need for banks and other middlemen from 20 to 65 percent. People will move towards a smarter era of trade.

Versatility in the Lending Options: It will be easier for people to get loans on their cryptocurrencies and vice versa. This will boost the economic activity on the crypto and blockchain platforms.

Now Here is the downside:

Volatility: The biggest challenge that the idea faces is the volatility of the cryptocurrency. People may hesitate to accept this new method due to reservations about the fluctuating market of cryptocurrency.

Cyber Risks: Fractional banking would be more prone to cyber-attacks. There is a higher risk that the scammers will use fake fractional reserve tokens. Another probability could be hijacking the DLT systems to launder money.

Regulatory Uncertainty: Much work still needs to be done on the regulatory environment of cryptocurrency. And when implementing fractional banking, a proper regulatory environment carries more importance.

Challenges of Technical System: Easier said than done. The technical system faces a lot of challenges. The challenges include but are not limited to liquidity management, security, and scalability risks. It will require a lot of back work before fractional banking empowered by DLTs could be introduced to the general public.

Conclusions:

Goldsmith came up with an innovative idea of fractional banking in the crypto world and the proposed model is very practical. But still much work needs to be done on the regulatory and security system. Also, the system faces scalability and technical challenges to make it a successful reality. If Goldman Sachs is able to successfully pass the obstacles. It will open new gateways of revolutionary changes for the cryptocurrency as well as the banking sector.