- Shares of crypto treasuries fell while token buys slowed

- Average BTC purchase size dropped to 343 coins in August

- Funding shifted toward loans as equity issuance faced limits

The Saylor Model frames a plain idea: treat Bitcoin as treasury and use the public equity wrapper to fund steady accumulation. The trade drew in small issuers that rebranded overnight and larger names that chased equity premia over spot holdings. Recent price action and flow data now test the approach in real time, as share declines, smaller ticket sizes, and tighter issuance terms unsettle a crowded field.

Saylor Model under market stress: prices, flows, and shrinking premia

A broad risk rally into an expected Federal Reserve cut has not lifted this corner. Architect Partners tracked 15 digital-asset treasury companies last week and found an average share decline of 15%. Several names moved far more. ALT5 Sigma, which holds the WLFI token tied to World Liberty Financial, fell about 50% in a little over a week. Kindly MD, which carries Bitcoin through a subsidiary, now sits around 80% below its May high. Ether- and Solana-linked wrappers also weakened, pulling down perceived net asset value and thinning the premium that once rewarded holders of the equity over the coins. Speculation still erupts in pockets. Eightco Holdings jumped more than 3,000% on Monday after it announced a Worldcoin-buying plan and added analyst Dan Ives to its board. The spike showed appetite for headlines in microcaps, yet it did little to change the group trend. With more than one hundred companies buying coins for treasury this year, often after a fast rebrand from unrelated lines like salons, cannabis, or marketing, the trade looks crowded. The Saylor Model needs steady access to equity capital and patient holders. Both look less certain when prices drift and liquidity fragments.

Funding pipelines tighten as issuance rules shift

The share-sale machine sits at the center of this model. Many issuers leaned on at-the-market programs to convert equity into Bitcoin without taking on term debt. That channel now faces friction. Nasdaq has reportedly asked some token-holding firms to seek shareholder approval before issuing new stock to fund purchases, which slows cadence and adds vote risk. Balance sheets pivoted toward bespoke financing as the equity window narrowed. Lenders, brokerages, and derivatives desks offered Bitcoin-backed loans, token-linked convertibles, and structured payouts. A London web studio, Smarter Web Co., even issued a bond pegged to Bitcoin rather than pounds, and limited the exposure to roughly 5% of its treasury. If Bitcoin rises, the amount owed rises too, which matches asset and liability but raises mark-to-market sensitivity. DDC Enterprise, once a meal company, disclosed more than $1 billion of available capacity across debt, equity lines, and shelf offerings, most of it untapped; its stock soared and then slumped within weeks, showing how authorizations can both enable quick adds and hang over shares. Two Prime reported rising demand from treasury firms for Bitcoin-backed loans between $10 million and $500 million, and said its active open loans stand near $1.25 billion. A fixed-maturity structure that defers monthly interest gives borrowers breathing room during volatility, but it can bunch liabilities later. The Saylor Model still works when capital arrives on time at sensible cost. Delays, votes, and wider spreads complicate that math.

Saylor Model metrics show a turn in Bitcoin buying

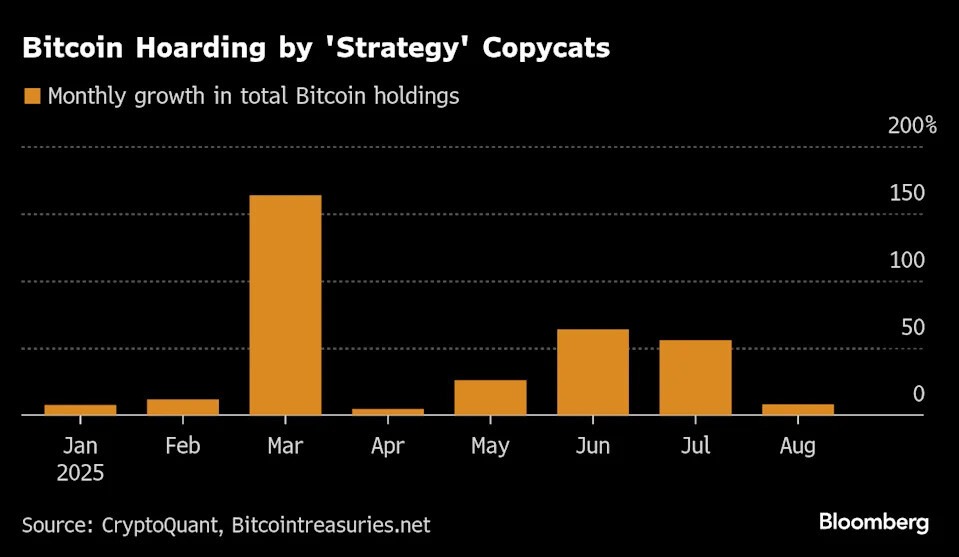

Flow data confirm cooling demand. According to CryptoQuant, digital-asset treasury firms bought about 14,800 Bitcoin in August, down from 66,000 in June. The average purchase size fell to 343 Bitcoin last month, an 86% drop from the 2025 peak. The accumulation rate slowed as well, moving from 163% growth in March to just 8% in August. Fewer coins, smaller tickets, and slower balance growth mean less support for equity premia, especially when operating cash flows do not cover the adds. The mix of participants also matters. In the United States, there are too many similarly positioned wrappers and too little differentiation on business model beyond holding tokens. That sameness blurs signals and pushes investors toward simpler paths like direct coins or ETFs. The Saylor Model can still create leverage when shares trade above net Bitcoin, yet dilution, fees, and working capital can erase that edge. As those pressures build, investors mark down the wrapper and compress the multiple to coins.

Winners, laggards, and the path ahead

Leaders set the tone as conditions shift. Strategy rallied earlier in the year but then stalled, and it was left out of the S&P 500 in Friday’s rebalance despite meeting eligibility screens. Since April, its stock went mostly sideways even as Bitcoin rallied, which pushed its market-cap-to-Bitcoin multiple, or mNAV, toward about 1.5. The company still bought roughly $217 million of Bitcoin on Monday through an at-the-market program, signaling continued use of equity for adds. Japan’s Metaplanet also cooled after gains, showing that geography does not shield the approach from sentiment. Across the field, more issuers talk about consolidation. Stronger balance sheets may target peers for their token books, while weaker players face higher financing costs and shrinking windows. Meanwhile, reported rules around shareholder approval will shape issuance calendars, index decisions will sway flows, and loan terms will define how much drawdown a treasury can absorb. For the Saylor Model to hold its place in public markets, per-share exposure needs to climb without heavy dilution, disclosures must track purchase cadence and funding mix in clear language, and managers must avoid liability structures that amplify volatility at the wrong time.

Conclusion

The Saylor Model remains the frame for many listed treasuries, but the easy phase has faded as crowding, rule frictions, and weaker premia weigh on shares. Last week’s 15-name basket fell an average of 15%, ALT5 dropped about 50% in a little over a week, and Kindly MD sits roughly 80% below its May high. CryptoQuant shows August buys at 14,800 Bitcoin versus 66,000 in June, average tickets at 343 coins, and the accumulation rate sliding from 163% in March to 8% in August. Funding now tilts toward Bitcoin-backed loans between $10 million and $500 million, with about $1.25 billion active, while headline moves like Eightco’s 3,000% pop remain outliers. Strategy missed the S&P 500, carries an mNAV near 1.5, and still added about $217 million via an at-the-market sale. The field’s outlook turns on cleaner balance sheets, steadier issuance paths, and per-share coin growth that does not rely on constant dilution, which is the only path for this approach to keep investor trust.

Disclaimer

The information provided in this article is for informational purposes only and should not be considered financial advice. The article does not offer sufficient information to make investment decisions, nor does it constitute an offer, recommendation, or solicitation to buy or sell any financial instrument. The content is opinion of the author and does not reflect any view or suggestion or any kind of advise from CryptoNewsBytes.com. The author declares he does not hold any of the above mentioned tokens or received any incentive from any company.

Featured image created by AI