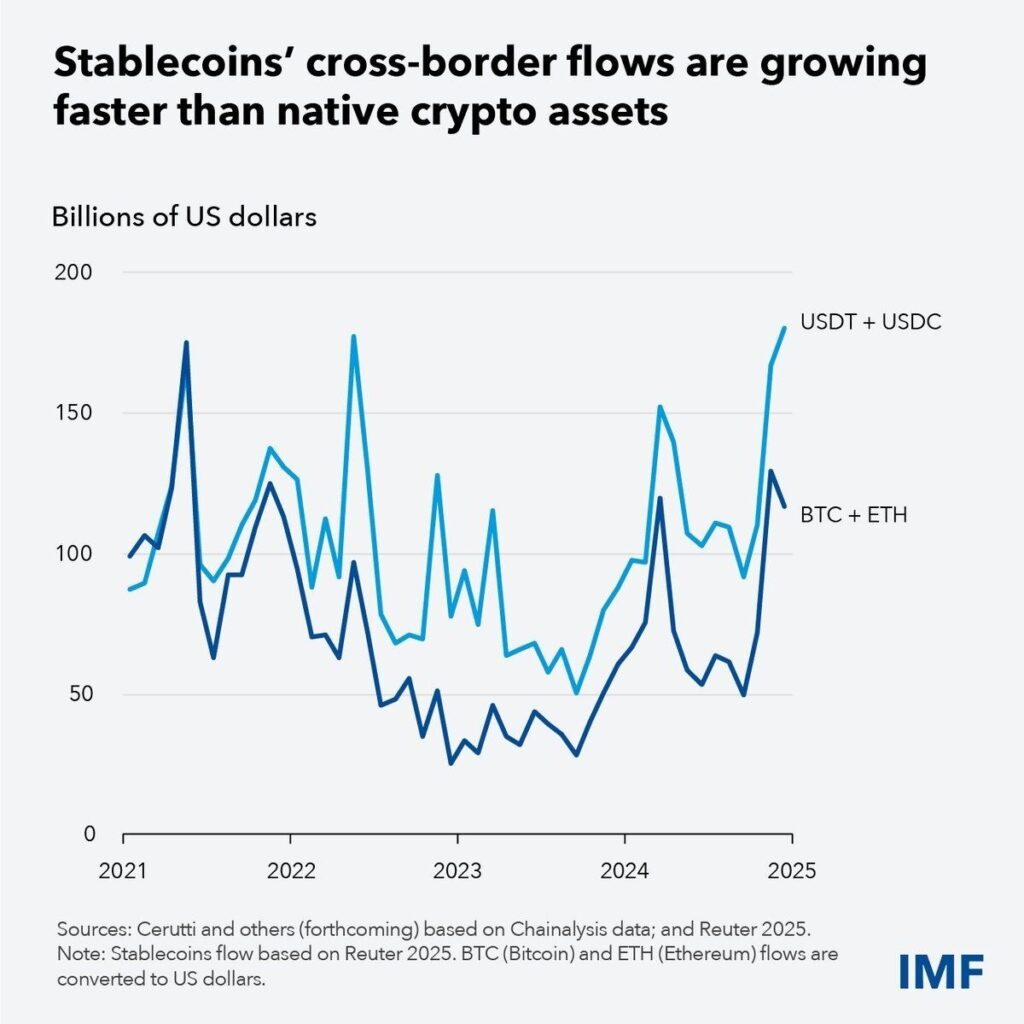

- Stablecoin flows now exceed Bitcoin and Ethereum cross-border activity

- IMF highlights risks for emerging market banks and currencies

- Report calls for clearer global rules on stablecoin reserves

Cross-border stablecoin flows reached fresh highs in 2025, surpassing those of Bitcoin and Ethereum for the first time, according to new data highlighted by the IMF. The shift marks a new phase in digital finance, where dollar-pegged tokens move more value across borders than the two largest native crypto assets combined. For the IMF, this is no longer a marginal development but a macro topic that touches exchange rates, capital flows, banking stability, and how people hold money in stressed economies. Total stablecoin issuance now exceeds 300 billion dollars and represents around 7% of all crypto assets, with Tether (USDT) and USD Coin (USDC) controlling more than 90% of the segment.

USDT’s circulating supply sits near 185.5 billion dollars, while USDC’s supply is about 77.6 billion dollars, cementing their role as the dominant digital dollar instruments on public blockchains. At the same time, a forthcoming IMF staff study maps roughly 2 trillion dollars of international stablecoin flows in 2024, showing that most of this activity crosses borders and often links regions with very different financial conditions. The IMF links these trends to a deeper pattern. Users in high-inflation or capital-controlled economies increasingly choose digital dollars via stablecoins instead of local currencies or domestic bank deposits. This preference may improve access to payment rails and savings tools, yet it also shifts monetary power away from local central banks and toward offshore issuers and global markets.

Stablecoin flows overtake Bitcoin and Ethereum in 2025

The latest figures show a decisive change in how value moves through crypto networks. Bitcoin and Ethereum once dominated cross-border flows, but stablecoins have now pushed ahead. In the IMF’s recent analysis, combined circulation for USDT and USDC has more than tripled in two years to about 260 billion dollars, while their trading volumes reached an estimated 23 trillion dollars in 2024, a rise of about 90% year on year. By contrast, flows in native assets have grown more slowly, which widens the gap between them and dollar-pegged tokens. This gap also appears in regional patterns. The IMF’s Crypto-Asset Monitor points to roughly 2 trillion dollars in gross stablecoin flows in 2024, with North America and Asia-Pacific posting the largest absolute volumes. Relative to GDP, however, Africa, the Middle East, Latin America, and the Caribbean stand out, with stablecoin flows reaching about 6.7% and 7.7% of GDP respectively, which underlines how important these instruments have become in smaller and more fragile economies. Asia has emerged as the leading region for stablecoin usage overall, according to the same research. Trading activity in Asia spans centralized exchanges, DeFi protocols, and cross-border transfers between businesses that pay suppliers or contractors in digital dollars. The United States and Europe remain major hubs, but the growth rate in several emerging regions outpaces that of developed markets when measured against economic size. These figures support a simple observation. Bitcoin and Ethereum still anchor the broader crypto market, yet stablecoins now carry more of the day-to-day liquidity, especially for remittances, trading, and short-term savings. In practice, much of the crypto ecosystem runs on tokenized dollars and similar reference currencies, even when investors still quote prices in BTC or ETH.

IMF warning reframes stablecoins as a macro-financial issue

The IMF does not describe this evolution as a temporary boom. In its latest publications and commentary, the institution frames stablecoins as a structural feature of the modern monetary system. The recent departmental work on cross-border flows stresses that stablecoins now function as a main driver of on-chain liquidity rather than a narrow settlement tool for speculative trades. In this reading, stablecoins sit at the intersection of payments, capital flows, and global demand for dollar assets. The IMF notes that most major stablecoins hold reserves in short-term US Treasury bills and similar instruments, which ties issuers directly into US money markets. Tether alone held nearly 98.5 billion dollars in Treasury bills by early 2025, equivalent to about 1.6% of all outstanding US T-bills, placing it alongside mid-sized sovereign investors. This structure generates what IMF economist Eswar Prasad calls a “stablecoin paradox.” Stablecoins reduce frictions in cross-border payments and improve access to digital savings products, yet they may reinforce the global role of the dollar and concentrate financial power in a small group of issuers and financial intermediaries.

The IMF links this dynamic to concerns over data transparency, governance, and the ability of authorities to monitor large and rapid shifts in dollar demand that take place outside the traditional banking system. The Fund also warns that rapid growth without consistent rules can raise volatility in capital flows. In times of market stress, households and firms may rush into or out of stablecoins, which could magnify swings in local currencies and create pressure on domestic funding conditions. These movements may occur within hours, because users need only a smartphone and an exchange account to shift balances between bank deposits, crypto wallets, and tokenized dollar instruments.

IMF concerns for emerging markets and banking systems

For many emerging markets, the IMF sees both advantages and risks in the new pattern of digital dollar usage. Stablecoins can lower the cost of remittances, which remain a vital income source for many low- and middle-income countries. They also allow savers in high-inflation environments to hold dollar-linked assets more easily, without passing through local banks that may offer negative real returns. At the same time, this ease of access can accelerate currency substitution. The IMF notes that in economies with weak institutions or strict capital controls, households and firms increasingly prefer digital dollars to local currency accounts. This behaviour can erode the domestic deposit base and limit the effectiveness of monetary policy tools, especially when central banks already face difficulties in anchoring inflation expectations. Research cited by the IMF, including analysis from Standard Chartered, estimates that stablecoins could pull as much as 1 trillion dollars in deposits away from emerging market banks if adoption continues to rise. Such an outflow would weaken local funding models, raise funding costs, and possibly push some institutions toward reliance on short-term wholesale markets. South Africa’s authorities have already highlighted this risk and described stablecoins as a potential threat to the financial stability of emerging-market banking systems. The Fund also stresses the problem of regulatory fragmentation. Major economies such as the United States, the European Union, and Japan now work on clearer stablecoin frameworks that specify reserve quality, redemption rights, and supervisory powers. Many emerging markets, however, still lack such rules or apply them only to a narrow set of licensed entities. As a result, stablecoin issuers may route activity through jurisdictions with lighter oversight, while users in stricter regimes continue to access tokens through offshore platforms. From the IMF’s perspective, this mismatch creates space for regulatory arbitrage and unmonitored liquidity accumulation. Authorities in weaker jurisdictions may see digital dollar balances grow inside their economies without having clear information on backing assets, redemption arrangements, or the stress behaviour of issuers. When sentiment reverses, rapid redemptions or shifts between tokens could add pressure to already fragile foreign-exchange markets.

Stablecoins, dollar dominance, and the coming policy roadmap

The latest warnings arrive as several international bodies study how stablecoins integrate into the wider monetary order. The IMF now treats these tokens as part of global liquidity conditions, not just as an internal detail of crypto markets. Its analysis connects stablecoin market caps, which often move ahead of broader crypto cycles, to future shifts in risk appetite, leverage, and cross-border dollar demand. A key issue is how stablecoins interact with dollar dominance. Most leading stablecoins remain dollar-referenced and hold reserves in US assets, especially Treasury bills and money-market instruments. This pattern strengthens the dollar’s role as a global store of value and unit of account, even in countries that attempt to diversify away from US currency exposure. In practice, the digital form of dollar assets extends the reach of US financial conditions into new segments of the global economy. The IMF’s Finance and Development articles and working papers outline several areas for policy design. They highlight the need for clear reserve disclosure, robust governance, and minimum capital standards for issuers that operate at scale. The Fund also supports close coordination between central banks and securities regulators on cross-border supervision, given that stablecoin liabilities can circulate far beyond the jurisdiction in which an issuer is domiciled. According to recent reporting, the IMF plans a more detailed policy roadmap for early 2026. This roadmap is expected to focus on three pillars: transparency standards for backing assets, frameworks for cross-border oversight, and common minimum safeguards for liquidity and capital. The aim is not to halt stablecoin development but to reduce the probability that digital dollar instruments trigger destabilizing runs or amplify stress in already fragile financial systems. For market participants, these debates suggest that regulation will move from broad principles to concrete requirements over the next few years. Stablecoin issuers may face stricter disclosure obligations and closer scrutiny of their investment portfolios, especially where holdings in government securities reach levels that matter for sovereign funding costs. At the same time, banks and payment firms in emerging markets will need to adapt to a world in which customers can shift into tokenized dollars within minutes, with low fees and global reach.

Conclusion

Stablecoin flows surpassing Bitcoin and Ethereum mark more than a change in crypto market structure; they signal a reconfiguration of how digital dollars move through the global system. The IMF treats this shift as a macro-financial issue because it touches exchange-rate regimes, capital-flow dynamics, and the resilience of banking systems in many regions. With total stablecoin issuance above 300 billion dollars, combined circulation of USDT and USDC near 260 billion dollars, and trading volumes around 23 trillion dollars in 2024, the scale now resembles that of mid-sized national financial systems rather than a niche corner of digital assets. For emerging markets, the same instruments that lower remittance costs and offer protection against inflation can also accelerate currency substitution and drain deposits from domestic banks. The IMF therefore calls for coordinated regulation that aligns reserve transparency, redemption rights, and supervisory tools across jurisdictions, while acknowledging the practical benefits that stablecoins provide to users. As the Fund prepares a more detailed policy roadmap for 2026, authorities face a limited window to shape how digital dollars integrate with existing frameworks before these tokens become a default medium for cross-border value transfer in many parts of the world.

Disclaimer

The information provided in this article is for informational purposes only and should not be considered financial advice. The article does not offer sufficient information to make investment decisions, nor does it constitute an offer, recommendation, or solicitation to buy or sell any financial instrument. The content is opinion of the author and does not reflect any view or suggestion or any kind of advise from CryptoNewsBytes.com. The author declares he does not hold any of the above mentioned tokens or received any incentive from any company.

Featured image created by AI