⚡ Key Highlights

- The GENIUS Act and MiCA are the two most important crypto regulatory frameworks in the world. Both require 1:1 reserve backing, redemption at par, and strict AML/KYC compliance. But they differ fundamentally in scope, structure, and enforcement

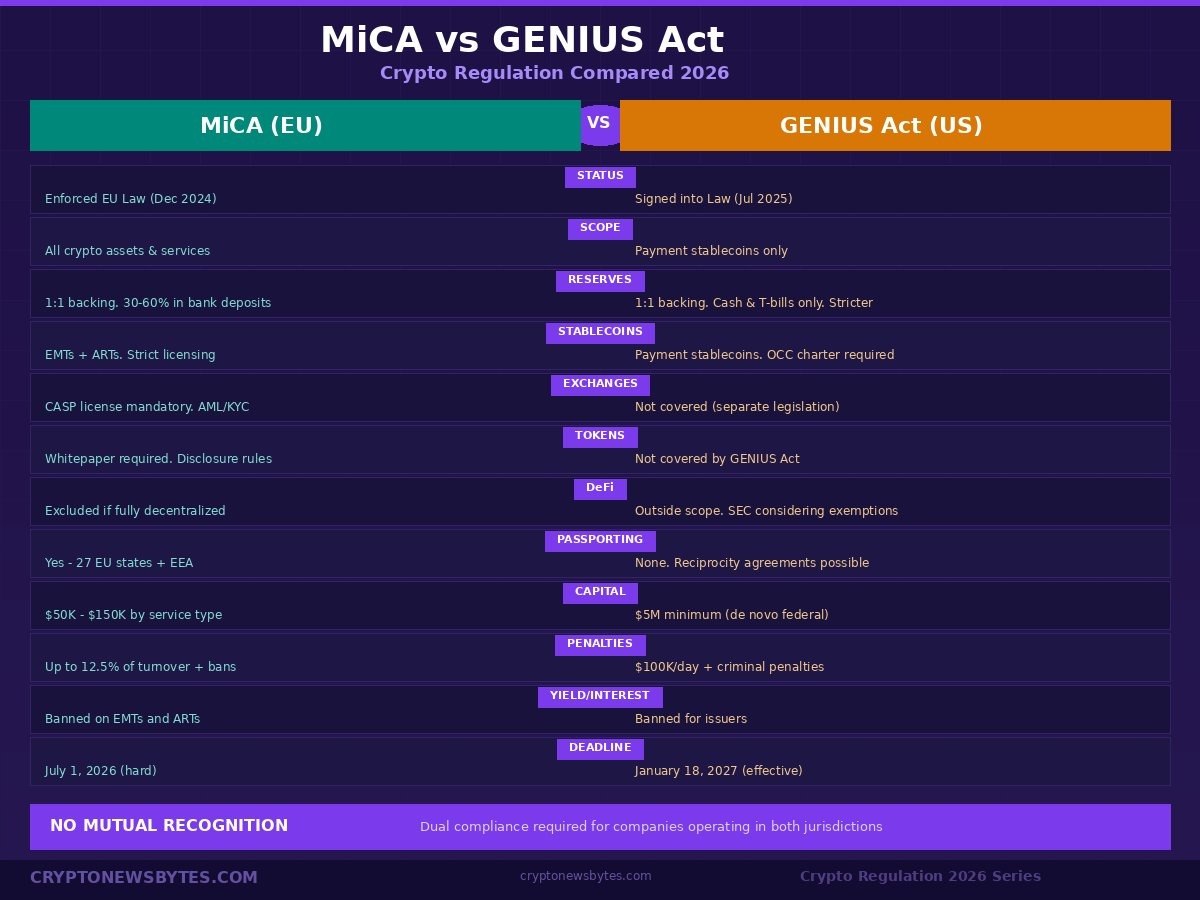

- MiCA covers all crypto assets and service providers across 27 EU member states. The GENIUS Act covers payment stablecoins only in the United States

- MiCA’s hard deadline is July 1, 2026. The GENIUS Act’s effective date is January 18, 2027. Companies operating in both markets face overlapping compliance windows

- There is no mutual recognition between the two frameworks. Global operators must maintain dual compliance, dual reserves, and dual licensing

- The GENIUS Act is more conservative on reserves than MiCA: it bans longer-maturity bonds and does not require reserves in banks (avoiding bank credit risk). MiCA requires 30-60% of reserves in bank deposits

- MiCA fines reach 12.5% of annual turnover for legal entities. The GENIUS Act imposes $100,000 per day for material breaches plus criminal penalties for willful misconduct

- MiCA offers EU-wide passporting (one license, 27 countries). The GENIUS Act has no passporting but encourages the Treasury to pursue international reciprocity agreements

- Both frameworks are creating a two-tier stablecoin market: compliant “constitutional cash” tokens vs non-compliant tokens that will be delisted from regulated exchanges

GENIUS Act vs MiCA: Why This Comparison Matters Now

If you operate a crypto business that serves customers on both sides of the Atlantic, the next 12 months will define your compliance architecture for years to come. The GENIUS Act vs MiCA comparison is not academic. It determines how you structure reserves, where you incorporate entities, which stablecoins you can list, and how much capital you need to hold.

Both frameworks were born from the same concern: stablecoins grew too large and too interconnected to remain unregulated. The collapse of TerraUSD in 2022 wiped out $40 billion and demonstrated what happens when algorithmic stablecoins fail without consumer protections. Both the U.S. and EU responded with legislation. But their approaches differ in ways that create real operational complexity for global companies.[World Economic Forum]

The GENIUS Act, signed into law on July 18, 2025, is the first U.S. federal framework for payment stablecoins. MiCA (Markets in Crypto-Assets Regulation, EU 2023/1114) took effect in phases starting June 2024, with full CASP enforcement arriving July 1, 2026. Together, these two regimes will govern the majority of global stablecoin activity. Understanding the GENIUS Act vs MiCA differences is now a baseline requirement for compliance teams at any serious crypto company.

The Master Comparison: GENIUS Act vs MiCA Side by Side

This table covers every major provision where the two frameworks align or diverge:

| Provision | GENIUS Act (United States) | MiCA (European Union) |

|---|---|---|

| Status | Signed into law Jul 18, 2025. OCC rulemaking in progress | Fully enacted. CASP regime live since Dec 30, 2024 |

| Scope | Payment stablecoins only | All crypto assets, stablecoins, and service providers |

| Hard deadline | Jan 18, 2027 (or 120 days after final rules) | Jul 1, 2026 (grandfathering expires) |

| Reserve requirement | 100% in cash, demand deposits, T-bills (93 days or less). No longer-maturity bonds | 100% in low-risk liquid assets. 30-60% must be in bank deposits (introduces bank credit risk) |

| Reserve segregation | Banks must issue from separate entity/balance sheet, insulated from core banking | No separate entity requirement for bank issuers |

| Redemption | At par, within 2 business days. Priority in bankruptcy | At par, at any time. Redemption right is constitutionalized |

| Yield/interest | Banned for issuers. Affiliate rewards under active debate | Banned for EMTs and ARTs |

| Licensing model | OCC federal charter, bank subsidiary, or state license (under $10B) | CASP authorization from National Competent Authority in any EU state |

| Passporting | None domestically. Treasury encouraged to pursue international reciprocity | Yes. One license covers all 27 EU states + EEA (450M customers) |

| Capital (minimum) | $5M for de novo federal issuers (floor, not ceiling) | $50K-$150K depending on CASP service type |

| Graduation threshold | $10B triggers mandatory federal oversight (360-day transition) | Significant ART/EMT issuers graduate to EBA co-supervision |

| Penalties | $100K/day civil fines. Criminal penalties for willful misconduct | Up to 12.5% of turnover. License revocation. Executive bans |

| Market abuse | Not addressed (separate legislation expected) | Comprehensive market abuse regime included |

| Algorithmic stablecoins | Banned. Study required for non-payment stablecoins | Cannot be marketed as “stablecoins.” Outside MiCA scope |

| DeFi treatment | Excluded from GENIUS Act scope. SEC considering exemptions for some DeFi | Excluded if “fully decentralized.” Assessment reports due 2025/2027 |

| Foreign issuers | Must register with OCC and hold U.S. reserves. Reciprocity possible | Must incorporate EU entity and obtain full CASP authorization |

| Disclosures | Monthly public + weekly confidential to regulators | Mandatory whitepapers + ongoing reporting to NCA and ESMA |

| Tax reporting | CARF implementation TBD. IRS crypto reporting rules in effect | DAC8 live Jan 1, 2026. Cross-border data exchange starts 2027 |

Where the Two Frameworks Converge

Despite their structural differences, the GENIUS Act vs MiCA comparison reveals several core principles where the two regimes are converging. This convergence is not coincidental. Both were influenced by the FSB’s High Level Recommendations on Global Stablecoin Arrangements and the G20 Crypto-Asset Policy Implementation Roadmap.[BVNK]

✅ Where They Agree

1:1 reserve backing is mandatory. Both frameworks require stablecoin issuers to hold reserves equal to 100% of outstanding tokens. Fractional reserves are prohibited.

Redemption at par value. In both jurisdictions, holders can redeem stablecoins for the equivalent fiat currency amount. The GENIUS Act specifies a two-business-day window. MiCA constitutionalizes redemption as a holder’s enforceable right.

Yield and interest are prohibited. Neither framework allows issuers to pay interest directly on payment stablecoins or e-money tokens.

AML/KYC is non-negotiable. Both require full compliance with anti-money laundering and know-your-customer rules. The GENIUS Act ties issuers to the Bank Secrecy Act. MiCA enforces the Transfer of Funds Regulation’s travel rule.

Graduation to higher oversight. Both frameworks escalate supervision as issuers grow. The GENIUS Act triggers federal oversight at $10 billion. MiCA escalates significant stablecoins to European Banking Authority co-supervision.

Where the Frameworks Fundamentally Diverge

The GENIUS Act vs MiCA differences become most apparent in five areas that directly affect how companies operate:

⚠️ Critical Differences

Scope. This is the most fundamental divergence. MiCA regulates the entire crypto ecosystem: exchanges, custodians, portfolio managers, advisors, transfer services, and token issuers. The GENIUS Act regulates only payment stablecoins. U.S. market structure regulation (exchanges, brokers, DeFi) is being addressed separately through the CLARITY Act, which is still moving through Congress.

Reserve composition. The World Economic Forum analysis highlights that the GENIUS Act is actually more conservative than MiCA on reserves. GENIUS prohibits longer-maturity bonds and does not require reserves to be held in bank deposits, avoiding the bank credit risk that MiCA introduces by mandating 30-60% of reserves in bank deposits. GENIUS also requires banks to issue stablecoins from a separate entity and balance sheet, insulating reserves from core banking operations. MiCA does not have this requirement.[WEF]

Passporting vs reciprocity. MiCA’s strongest competitive advantage is EU-wide passporting: one license grants access to 450 million customers across 27 countries. The GENIUS Act has no domestic passporting (the state/federal split remains). However, GENIUS goes further than MiCA on international reciprocity by empowering the Treasury to negotiate bilateral agreements with “comparable jurisdictions,” potentially allowing U.S.-licensed issuers to serve foreign markets without full local licensing.

Enforcement. MiCA has a broader enforcement toolkit. Beyond financial penalties, it directly addresses market abuse (insider trading, market manipulation) for crypto assets. As of late 2025, MiCA enforcement has already produced over 540 million euros in fines and more than 50 license revocations. The GENIUS Act does not address market abuse (that will come in separate legislation) but does introduce criminal penalties for willful misconduct, something MiCA leaves to member state discretion. For a full breakdown of GENIUS Act penalties and OCC rulemaking, see our complete GENIUS Act guide.[WH Partners]

Foreign issuer treatment. Both require foreign issuers to comply, but the paths differ. MiCA requires foreign companies to incorporate an EU entity and obtain full authorization. The GENIUS Act requires registration with the OCC and U.S.-based reserves, but opens the door for reciprocity waivers if the issuer’s home jurisdiction has a “substantially similar” regime.[WH Partners]

GENIUS Act vs MiCA: Impact on Stablecoins

The stablecoin market is where the GENIUS Act vs MiCA comparison has the most immediate practical consequences. Both frameworks are creating what industry analysts call a “two-tier” stablecoin market: compliant tokens that can operate on regulated exchanges, and non-compliant tokens that face delisting and marginalization.[TronWeekly]

| Stablecoin | GENIUS Act Status | MiCA Status |

|---|---|---|

| USDC (Circle) | Positioned for compliance | MiCA-licensed EMI in France |

| EURC (Circle) | N/A (euro-denominated) | MiCA-compliant |

| USDT (Tether) | Compliance path unclear | Non-compliant, being delisted |

| PYUSD (PayPal) | Positioned for compliance | EU status TBD |

| Bank-issued stablecoins | 5 OCC charters approved | QiValis consortium (12 EU banks) launching H2 2026 |

| Algorithmic stablecoins | Banned | Cannot be marketed as stablecoins |

The most significant GENIUS Act vs MiCA market impact centers on Tether’s position. USDT remains the world’s largest stablecoin by market cap, but it is non-compliant with MiCA and faces an uncertain compliance path under the GENIUS Act. EU exchanges have already started delisting USDT. If USDT cannot achieve compliance under the GENIUS Act by January 2027, U.S. exchanges will face the same pressure. Circle’s USDC and the emerging generation of bank-issued stablecoins are the clearest beneficiaries of both regulatory regimes.

Regulatory Oversight: Who Has Power Under Each Framework

One of the most practical GENIUS Act vs MiCA differences is in who actually supervises crypto companies. The oversight structures reflect fundamentally different governance models.

| Function | GENIUS Act (US) | MiCA (EU) |

|---|---|---|

| Primary stablecoin regulator | OCC (federal charter issuers) | National Competent Authority in home member state |

| Bank-issued stablecoins | FDIC (state nonmember), Federal Reserve (state member), OCC (national) | National banking regulator + NCA |

| Systemically important issuers | Federal Reserve, OCC, or NCUA (triggered at $10B) | European Banking Authority (EBA) co-supervision |

| Exchange/service provider oversight | Not covered by GENIUS Act (SEC/CFTC under separate legislation) | NCA in home state + ESMA coordination |

| AML/KYC enforcement | FinCEN under Bank Secrecy Act | NCAs + Transfer of Funds Regulation (travel rule) |

| Market abuse | Not addressed (expected in future legislation) | ESMA-coordinated, includes insider dealing and market manipulation |

The U.S. system spreads authority across multiple agencies: the OCC for federal stablecoin issuers, the FDIC and Federal Reserve for bank subsidiaries, FinCEN for anti-money laundering, and the SEC and CFTC for broader market structure (under separate legislation). The EU centralizes crypto oversight through National Competent Authorities supervised by ESMA at the EU level, with the EBA handling significant stablecoin issuers. For a detailed breakdown of U.S. agency roles, see our GENIUS Act guide.

Compliance Burden: What Crypto Companies Actually Need to Do

For founders, compliance teams, and exchanges, the operational reality of each framework is what matters most. Here is how the day-to-day compliance requirements compare:

| Requirement | GENIUS Act (US) | MiCA (EU) |

|---|---|---|

| Licensing process | OCC national trust bank charter application, or state license (under $10B) | CASP authorization from NCA. Application can be hundreds of pages |

| Whitepaper requirement | No formal whitepaper mandate (disclosures required via OCC rules) | Mandatory crypto-asset whitepaper with detailed risk, tech, and functionality disclosures |

| Reserve disclosures | Monthly public + weekly confidential to regulators | Ongoing to NCA + ESMA register. Quarterly audits for stablecoins |

| AML/KYC | Full Bank Secrecy Act compliance. FinCEN to write tailored AML rules | Transfer of Funds Regulation travel rule. Sender/recipient data for every transfer |

| Client asset segregation | Banks must issue from separate entity and balance sheet | CASPs must segregate client assets from company funds. Daily reconciliation |

| Wallet/custody providers | Banks permitted to custody stablecoins and reserve assets | Custody is a licensed CASP service ($150K capital). Client fiat must go to EU credit institution by next business day |

| Tax reporting | IRS crypto reporting rules. CARF implementation timeline TBD | DAC8 live since Jan 1, 2026. Cross-border data exchange starts 2027 |

MiCA’s whitepaper requirement is one of the most notable operational differences. Every crypto asset offered to the public or listed on a trading platform in the EU must have a published whitepaper detailing functionality, risks, technology, issuer governance, and redemption rights. The GENIUS Act does not mandate a formal whitepaper, though the OCC’s proposed rules include extensive disclosure requirements. For MiCA’s full CASP licensing requirements and capital thresholds, see our dedicated guide.

Innovation vs Regulation: Two Different Philosophies

The GENIUS Act vs MiCA debate is ultimately a reflection of two different regulatory philosophies toward crypto innovation.

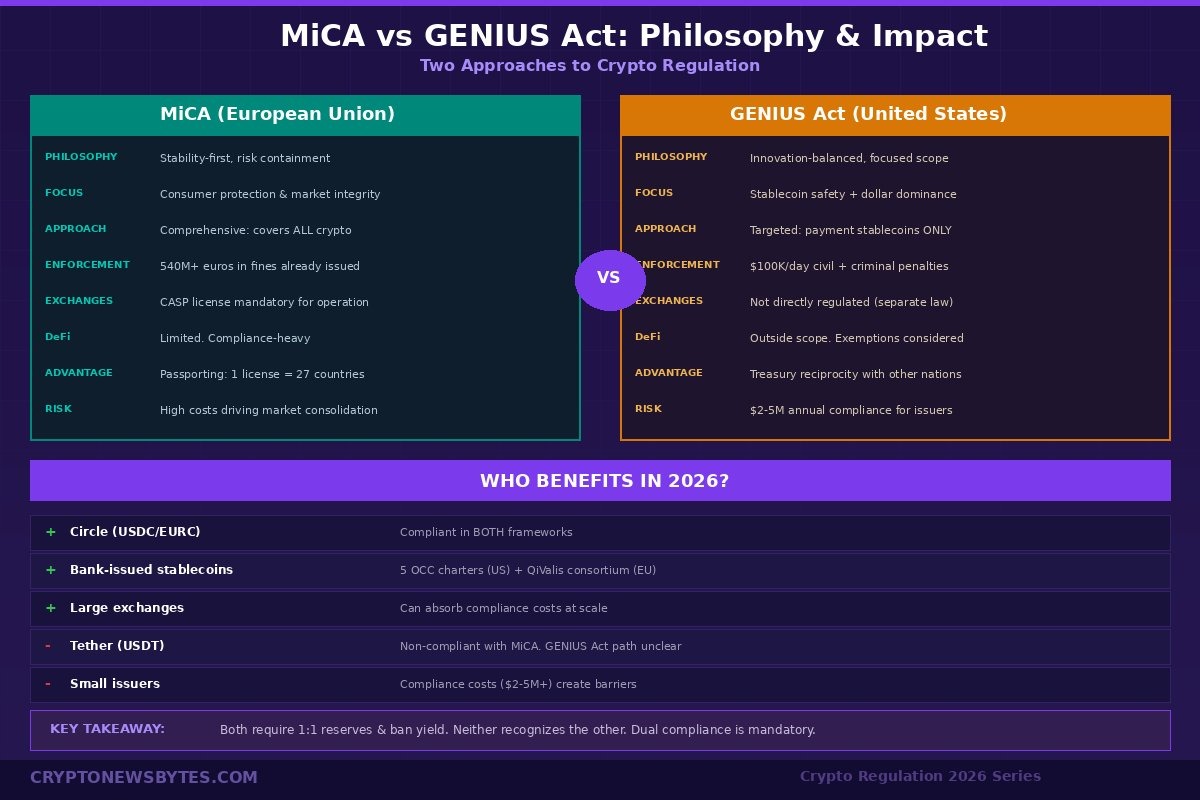

The EU approach under MiCA is stability-first. MiCA was designed to contain systemic risk, protect consumers, and prevent the kind of unregulated growth that led to the TerraUSD collapse. It treats crypto assets as a potential threat to financial stability that must be contained within existing regulatory architecture. Innovation is permitted but only within the boundaries of comprehensive licensing, disclosure, and conduct rules. The result: compliance costs are high, but legal certainty is unmatched. MiCA’s passporting system creates a genuine single market for compliant crypto businesses, which is itself a form of innovation incentive.

The U.S. approach under the GENIUS Act is innovation-balanced. The GENIUS Act was crafted as a bipartisan compromise that provides guardrails without stifling growth. By focusing exclusively on payment stablecoins (rather than all crypto assets), it deliberately leaves room for the broader market to develop before imposing comprehensive rules. The CLARITY Act (market structure) and additional legislation are expected to fill the gaps. The philosophy is clear: define the most critical category first (stablecoins), set strict reserve and consumer protection standards, and allow the rest of the ecosystem to mature. Treasury Secretary Scott Bessent has publicly framed regulated stablecoins as a tool for financing U.S. government debt, suggesting the law serves strategic economic interests beyond consumer protection.[Bitwage]

Neither approach is objectively “better.” The EU offers immediate legal certainty at the cost of higher compliance burden and reduced flexibility. The U.S. offers focused clarity on stablecoins with a lighter touch elsewhere, but leaves uncertainty for exchanges, DeFi, and token issuers until additional legislation passes.

Global Market Impact: Will Companies Choose the EU or US?

The GENIUS Act vs MiCA competition is reshaping where crypto companies choose to incorporate, where they hold reserves, and which markets they prioritize.

MiCA is driving consolidation in Europe. The compliance costs and licensing requirements have created barriers to entry for smaller issuers. Georgetown Law research noted that many smaller EU companies are merging with larger firms to absorb regulatory costs, reducing market fragmentation but also raising concerns about reduced diversity and innovation. More than 50 firms had licenses revoked by early 2025 for failing to meet AML or reserve requirements.[Georgetown Law]

The GENIUS Act may attract global stablecoin issuers to the U.S. The law’s reciprocity provisions are unique. By empowering the Treasury to negotiate bilateral recognition agreements with comparable jurisdictions, the GENIUS Act creates a path for U.S.-licensed issuers to serve international markets with home-regulator backing. If Treasury reaches reciprocity agreements with the EU, UK, or Singapore, U.S.-based issuers could gain a competitive advantage that MiCA’s framework does not currently offer in the other direction.[WEF]

Bank-issued stablecoins are emerging in both jurisdictions. In the U.S., five OCC national trust bank charters have been conditionally approved. In the EU, the QiValis consortium of 12 major European banks (including BBVA) is building a MiCA-regulated euro stablecoin for launch in H2 2026. This convergence suggests that the ultimate winners in both markets may be established financial institutions rather than crypto-native firms.[TronWeekly]

The global trend is clear: stablecoin regulation is converging on core principles (1:1 reserves, licensing, AML/KYC, redemption rights) while differing in scope and philosophy. Companies that build compliance into their infrastructure from day one will be positioned to operate across both regimes. Those that delay risk being locked out of one or both of the world’s largest regulated crypto markets.

What the GENIUS Act vs MiCA Comparison Means for Investors

Stablecoin safety is dramatically improved under both frameworks. Before the GENIUS Act and MiCA, stablecoin holders had no statutory guarantee that reserves existed, that redemption would be honored, or that issuers would survive a bank run. Both frameworks now provide enforceable redemption rights at par value, mandatory 1:1 reserve backing, and regulatory oversight of reserve composition. For investors, this transforms stablecoins from trust-based instruments into legally protected ones.

Exchange risk is being reduced but not eliminated. MiCA requires exchanges to segregate client assets, maintain business continuity plans, and undergo regular audits. The GENIUS Act does not directly regulate exchanges, but by requiring that only compliant stablecoins can be listed, it creates indirect pressure for exchanges to maintain higher standards. The combination of MiCA’s direct exchange oversight and the growing crypto insurance market is creating a safety infrastructure that did not exist two years ago.

Cross-border investing becomes clearer but not simpler. Investors holding compliant stablecoins can now assess issuer risk based on published reserve disclosures and regulatory status rather than trust alone. However, the lack of mutual recognition between the GENIUS Act and MiCA means that a stablecoin compliant in one jurisdiction may not be available in the other. USDT’s EU delisting is the most visible example. Investors should monitor which stablecoins maintain dual compliance (USDC currently leads) and adjust holdings accordingly.

Token issuance transparency is improving but unevenly. MiCA’s mandatory whitepaper requirement means that every token listed on EU exchanges must have published disclosures covering technology, risks, and governance. The GENIUS Act does not impose equivalent requirements for tokens other than payment stablecoins. Investors active in both markets will find significantly more disclosure available for EU-listed tokens than for U.S.-listed tokens outside the stablecoin category.

What the GENIUS Act vs MiCA Comparison Means for Your Business

If you operate in the U.S. only: The GENIUS Act is your primary framework, but watch MiCA closely. Many U.S. companies serve EU customers (even indirectly), and MiCA’s extraterritorial reach means you may need authorization. The GENIUS Act’s reciprocity provisions could eventually simplify cross-border compliance, but no agreements exist yet.

If you operate in the EU only: MiCA is your compliance priority. Our MiCA compliance guide covers CASP licensing, capital requirements, and grandfathering deadlines in detail. The GENIUS Act matters if you list any USD-denominated stablecoins, since issuers must comply with GENIUS to remain available on U.S. exchanges. If your customers trade USDC or USDT, the GENIUS Act’s rules indirectly affect your stablecoin offerings.

If you operate globally: You need dual compliance. The practical approach is to build to the stricter standard on each provision. For reserves, this means the GENIUS Act standard (no bank deposit concentration). For market conduct, this means MiCA’s market abuse regime. For licensing, you need both: an OCC charter or bank subsidiary for the U.S. and a CASP authorization for the EU. There is no shortcut. Budget for separate compliance programs, reserve structures, and regulatory relationships in both jurisdictions.

If you issue stablecoins: The combined annual compliance cost under both regimes is estimated at $2-5 million for mid-sized issuers, not including initial capital requirements. This cost barrier favors large, well-capitalized issuers. If you are a smaller issuer, consider the state pathway under the GENIUS Act (under $10B) or a single EU jurisdiction for MiCA, and scale from there.

If you invest in crypto: Both frameworks dramatically improve the safety profile of regulated stablecoins. Compliant tokens now have enforceable reserve backing, redemption rights, and regulatory oversight comparable to traditional financial instruments. This matters for institutional allocation decisions and directly affects crypto insurance eligibility.

Frequently Asked Questions

📰 Crypto Regulation 2026 Series

- The GENIUS Act Explained: What Every Crypto Company Needs to Know in 2026

- MiCA Regulation 2026: The Complete Compliance Guide for Crypto Companies

- You are here: GENIUS Act vs MiCA: The Complete Comparison for Crypto Companies

- Coming next: SEC vs CFTC: Who Regulates What in Crypto After the CLARITY Act

🔒 Security & Insurance Series

- Crypto Insurance in 2026: Why the Industry’s Biggest Problem Is Not Hackers

- Best Crypto Insurance Providers in 2026 Compared

- $2.72B Stolen in 2025: The Crypto Insurance Lessons Every Founder Needs

- Figure Technology Data Breach: Hackers Dump 2.5GB Stolen Records

- Step Finance Hack: $40M Stolen, Platform Shuts Down

- Top 10 Cybersecurity Trends in Crypto & Blockchain 2025

Sources: World Economic Forum | TronWeekly | BVNK | WH Partners | Bird & Bird | Georgetown Law | eu.ci | Chainstack | Bitwage | Stablecoin Insider | ESMA | KuCoin

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or regulatory advice. Both the GENIUS Act and MiCA frameworks are actively evolving through rulemaking and enforcement. All information is based on publicly available sources as of March 1, 2026. Consult qualified legal counsel in the relevant jurisdiction for advice specific to your business.