📋 In This Guide

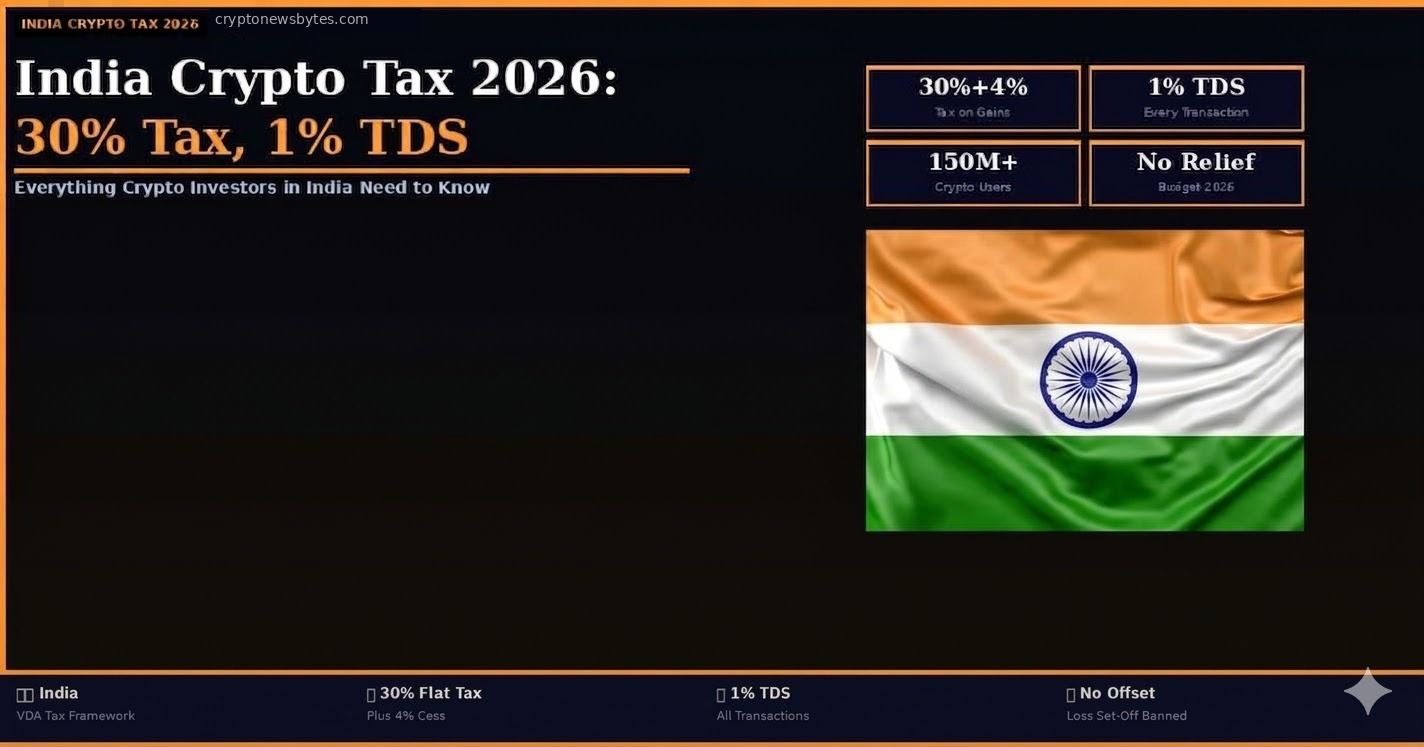

- India Crypto in 2026: Legal, Taxed, and Controversial

- The 30% VDA Tax: How It Works Under Section 115BBH

- The 1% TDS: Every Transaction, Every Time

- No Loss Set-Offs: The Most Punishing Rule

- Real Tax Math: What a ₹10 Lakh Gain Actually Costs You

- Budget 2026: What Changed (and What Did Not)

- How to File Crypto Taxes in India 2026

- FAQ

⚡ Key Takeaways — India Crypto Tax 2026

- India taxes all Virtual Digital Asset (VDA) profits at a flat 30% rate under Section 115BBH, plus a 4% health and education cess, regardless of holding period or income level.

- A 1% Tax Deducted at Source (TDS) applies under Section 194S to every transfer of a VDA exceeding the threshold, deducted at the time of transaction by exchanges or the buyer in P2P trades.

- No loss set-offs are permitted. Losses from selling one cryptocurrency cannot offset gains from another, cannot be offset against stock or other income, and cannot be carried forward.

- The Budget 2026-27 kept the 30% rate and 1% TDS unchanged, despite months of industry lobbying for reduction, disappointing exchanges and traders who had hoped for reform.

- New penalties take effect from April 1, 2026: reporting entities failing to submit required crypto transaction statements face ₹200 per day in fines, plus a flat ₹50,000 penalty for inaccurate disclosures.

- India has 150+ million crypto users and the highest global crypto adoption rate by transaction volume (Chainalysis 2025), yet an estimated 70%+ of trading volume happens on offshore platforms due to tax friction.

India holds a paradox in global crypto. It has more crypto users than almost any other country in the world. Its Supreme Court struck down the RBI’s banking ban in 2020, making crypto legal. Its government officially recognised digital assets as Virtual Digital Assets in the 2022 Union Budget, giving them legal status under the Income Tax Act. And yet India also has arguably the most punishing crypto tax regime of any major economy: a 30% flat tax on every gain, a 1% TDS on every transaction, no ability to set losses against gains, no distinction between short-term and long-term holdings, and no relief in the 2026 budget. The consequence is predictable. Hundreds of billions in trading volume has migrated to offshore platforms, shrinking the domestic industry and the government’s own tax base.

India Crypto in 2026: Legal, Taxed, and Controversial

Crypto is legal to buy, hold, sell, and trade in India. Bitcoin, Ethereum, and other cryptocurrencies are recognized as Virtual Digital Assets under Section 2(47A) of the Income Tax Act, inserted by the Finance Act 2022. Regulated exchanges including WazirX, CoinDCX, CoinSwitch, and ZebPay operate in India and are registered with the Financial Intelligence Unit (FIU). The Financial Intelligence Unit registration is the primary compliance obligation for crypto exchanges today, covering AML, KYC, and suspicious transaction reporting, but does not constitute a full regulatory license. SEBI, India’s securities regulator, has explored taking jurisdiction over crypto exchanges, but as of early 2026, no formal regulatory framework has been implemented.

The RBI continues to view private cryptocurrencies with caution, regularly warning about financial stability risks, but it no longer has the ability to impose a banking ban. Banks serve crypto exchanges, though some remain cautious in practice. The e-Rupee digital currency launched by the RBI in 2022 is in advanced rollout by 2026 but has not displaced demand for Bitcoin, Ethereum, or stablecoins among Indian investors.

The 30% VDA Tax: How It Works Under Section 115BBH

Section 115BBH of the Income Tax Act imposes a flat 30% tax on income from the transfer of any Virtual Digital Asset. The rate applies regardless of the investor’s income bracket, the holding period of the asset, or whether the gain is short-term or long-term. There is no indexation benefit, no benefit from long-term capital gains rates, and no reduced rate for any category of crypto asset.

The only deduction permitted is the cost of acquisition. Exchange fees, transaction costs, gas fees, mining costs, hardware wallet expenses, and any other costs associated with acquiring or disposing of the asset cannot be deducted. The tax is computed purely on the difference between disposal proceeds and acquisition cost. On top of the 30% base rate, a 4% health and education cess applies, making the effective rate 31.2% for most individual investors, rising with surcharges for high-income taxpayers.

| Income Level | Base Tax | Surcharge | Cess | Effective Rate |

|---|---|---|---|---|

| Up to ₹50 lakh | 30% | Nil | 4% | 31.2% |

| ₹50L — ₹1 crore | 30% | 10% | 4% | 34.32% |

| ₹1Cr — ₹2 crore | 30% | 15% | 4% | 35.88% |

| Above ₹2 crore | 30% | 25% | 4% | 39% |

The 1% TDS: Every Transaction, Every Time

Section 194S requires a 1% TDS to be deducted at source on every transfer of a VDA where the transaction value exceeds ₹50,000 in a financial year (or ₹10,000 for specified persons). On registered Indian exchanges, this is deducted automatically by the platform. For peer-to-peer trades, international exchange trades, and over-the-counter transactions, the buyer is responsible for deducting and depositing the TDS with the government, a compliance burden that most retail traders struggle to manage correctly.

The TDS is not an additional tax: it is advance tax that can be credited against the final 30% tax liability at year-end. But for high-frequency traders and market makers, a 1% TDS on every transaction destroys profitability regardless of ultimate tax liability. A trader making 100 trades per month with ₹1 lakh per trade faces ₹1 lakh in TDS deductions per month, tying up capital that may not be recovered until an annual tax refund. This is the primary driver of volume migration to offshore platforms, where no TDS is deducted.

No Loss Set-Offs: The Most Punishing Rule

The provision in Section 115BBH explicitly prohibiting loss set-offs is the feature that most distinguishes India’s crypto tax regime from every comparable jurisdiction. Under Indian tax law, a loss from selling Bitcoin cannot be used to reduce a gain from selling Ethereum, even within the same financial year. Losses on one VDA transaction cannot offset gains on another VDA transaction. And VDA losses cannot offset income from any other source including salary, business income, or gains from stocks and mutual funds.

Real Tax Math: What a ₹10 Lakh Gain Actually Costs You

Budget 2026: What Changed (and What Did Not)

India’s Union Budget 2026-27 was presented by Finance Minister Nirmala Sitharaman on February 1, 2026. The crypto industry mounted its strongest coordinated lobbying effort to date, with exchanges, trade bodies including BACC and IAMAI, and international platforms calling for TDS reduction from 1% to 0.01%, loss set-off permissions, and a move toward capital gains treatment for long-term holdings. None of these changes were made. The 30% tax rate and 1% TDS are unchanged.

What the budget did change: new penalties for reporting failures under Section 509 of the Income Tax Act, effective April 1, 2026. Entities required to file crypto transaction statements face a ₹200-per-day fine for each day of non-filing, and a flat ₹50,000 penalty for inaccurate or uncorrected information. The government is tightening compliance reporting while leaving the underlying tax structure untouched. Industry leaders have called the approach counterproductive, arguing the current framework drives users offshore and reduces the government’s visibility and tax collection rather than increasing it.

How to File Crypto Taxes in India 2026

Crypto gains must be reported under Schedule VDA in the Income Tax Return. Taxpayers with crypto income should file using ITR-2 (if salaried without business income) or ITR-3 (if with business income). Each transaction must be recorded with the date of acquisition, cost of acquisition in INR, date of disposal, and disposal proceeds in INR. TDS deducted by exchanges appears in Form 26AS and can be claimed as credit against tax liability.

| Event | Taxable? | Tax Treatment |

|---|---|---|

| Selling crypto for INR | Yes | 30% + cess on gain; 1% TDS |

| Swapping crypto for crypto | Yes | 30% + cess on gain at swap; 1% TDS |

| Spending crypto on goods | Yes | 30% + cess on disposal gain |

| Staking rewards received | Yes | Income tax at slab rate on receipt |

| Airdrop tokens received | Yes | Income tax at slab rate on receipt value |

| Mining income | Yes | Income tax at slab rate as business income |

| Gifting crypto to spouse | No (in giver’s hands) | Recipient taxed on eventual sale |

| Transferring between own wallets | No | No disposal event |

| Holding unrealised gains | No | Tax only on disposal |