What Just Happened

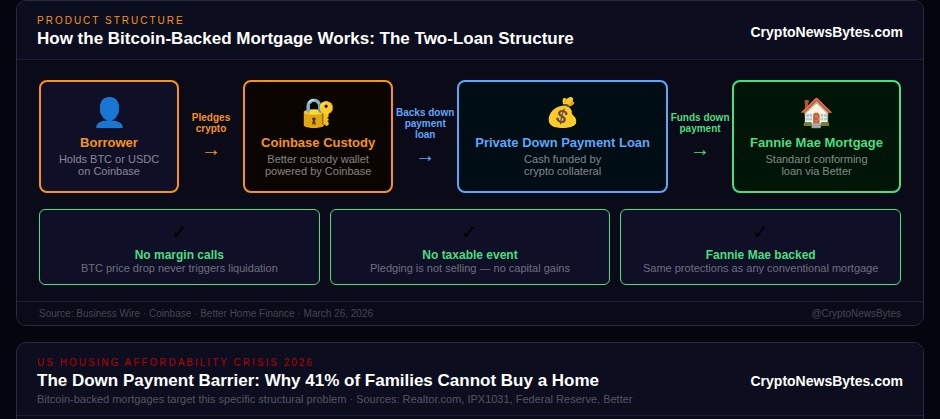

- Coinbase and Better Home and Finance have launched the first Bitcoin-backed conforming mortgage approved by Fannie Mae, allowing Americans to pledge Bitcoin or USDC as down payment collateral without selling their crypto

- No margin calls, no top-ups. If Bitcoin drops in value after pledging, the mortgage terms remain unchanged. Market movements alone never trigger liquidation. Collateral is only at risk if the borrower falls 60 days behind on payments

- 52 million Americans own digital assets. Better estimates it may have originated up to $40 billion more in mortgages had it accepted crypto collateral earlier

- Rates will run 0.5 to 1.5 percentage points above a standard 30-year mortgage depending on borrower profile. USDC pledgers can continue earning yield on their collateral, effectively reducing their net interest rate

- This is not a niche product. Backed by Fannie Mae and structured as a standard conforming loan, it carries the same protections as any conventional mortgage and is available to regular homebuyers, not just the wealthy

Bitcoin mortgage 2026 is now real. On March 26, 2026, Coinbase and Better Home and Finance launched the first token-backed conforming mortgage approved by Fannie Mae, the government-sponsored enterprise that underpins approximately $4 trillion of the US mortgage market. For the 52 million Americans who own digital assets, this changes the calculus of homeownership entirely. They no longer have to choose between their crypto and their home. They can pledge one to buy the other.

The US housing market is a $12 trillion asset class defined by a single structural problem: the down payment. It would take a median-income American household approximately 7 years to save for a typical down payment at current savings rates, according to Realtor.com data. Meanwhile, median home prices sit at $429,189 and 62% of Americans say buying a home in 2026 feels unrealistic. The down payment barrier has been the primary reason 41% of American families fail to purchase homes even when they hold other forms of wealth. This product targets that barrier directly.

How It Actually Works: The Five-Step Structure

The Problem This Solves: The $12 Trillion Housing Market’s Structural Barrier

To understand why this product matters, you need to understand the scale of the problem it is addressing. The US housing market is valued at approximately $12 trillion. It is the single largest asset class available to ordinary Americans and the primary vehicle through which middle-class wealth is built and transferred across generations. And it is increasingly inaccessible.

The median down payment in the US reached $30,400 in 2025, representing 14.4% of the purchase price. At a median savings rate, a typical household needs approximately 7 years to accumulate that amount. During those 7 years, home prices continue rising, savings rates underperform inflation, and the goalposts keep moving. Prospective homebuyers need an additional $200,000 compared to a decade ago to close on a median-priced property.

The down payment barrier is not distributed equally. Among renters who do not own, the most commonly cited barriers are inability to afford a down payment and inability to qualify for a mortgage, according to the Federal Reserve’s Report on Economic Well-Being of US Households. Black mortgage applicants face a denial rate of 21%, Hispanic applicants 17%, compared to 11% for White applicants. The average age of first-time buyers has now reached 40 years old.

Who Can Use This: The 52 Million American Crypto Holders

Approximately 52 million Americans, roughly 20% of adults, own digital assets according to the press release. This is not a niche group. It skews young: 75% of token holders are 35 years old or younger, and 26% earn less than $75,000 annually. These are exactly the demographics that have been most locked out of the housing market by the down payment barrier. The generational overlap is precise: the people who bought Bitcoin and Ethereum in 2019, 2020, and 2021 are now in their prime homebuying years and sitting on significant unrealised gains they cannot access without triggering a taxable event.

Better’s CEO Vishal Garg made the missed opportunity explicit: if Better had accepted crypto as down payment collateral in prior years, “we would have funded maybe $40 billion more of consumer demand over the past few years.” That is a single company’s estimate of suppressed demand from one structural barrier. Across the industry, the number is likely a multiple of that figure.

| Crypto Holder Profile | Detail | Relevance to Mortgage Product |

|---|---|---|

| Total US crypto holders | ~52 million (20% of adults) | Full addressable market |

| 75% are under 35 | Prime first-time homebuying age | Maximum overlap with down payment barrier demographic |

| 26% earn under $75K | Lower-income holders | Most affected by the down payment barrier |

| 12.7% of Gen Z and Millennials | Already sold tokenised assets to fund a down payment | Product would have prevented a forced taxable event |

| 3.5% of Gen X and 0.5% of Baby Boomers | Already used crypto for a down payment | Early adoption concentrated in younger generations |

The Cost: What Does a Bitcoin Mortgage Actually Cost?

The product is not free. Rates run between 0.5 and 1.5 percentage points above a standard 30-year mortgage, depending on the borrower’s profile. With the national average 30-year fixed rate currently at 6.0%, a Bitcoin-backed mortgage would cost approximately 6.5% to 7.5% in its initial structure.

| Scenario | Rate | Monthly Payment (on $400K loan) | Annual Premium Cost |

|---|---|---|---|

| Standard 30-year mortgage | 6.0% | ~$2,398 | Baseline |

| Bitcoin mortgage (low premium) | 6.5% | ~$2,528 | +$1,560/yr |

| Bitcoin mortgage (high premium) | 7.5% | ~$2,797 | +$4,788/yr |

| USDC mortgage (with yield offset) | 6.5% minus yield | Lower than stated rate | Net cost depends on USDC yield |

The premium is real but must be weighed against the alternative: selling Bitcoin to fund the down payment, triggering a capital gains tax event on unrealised appreciation. For someone who bought Bitcoin at $10,000 and is now using it as collateral at $74,784, the capital gains tax liability on a sale would far exceed the mortgage premium in most cases. Keeping the Bitcoin and paying the premium is the rational financial choice for anyone with meaningful unrealised gains.

Coinbase One members who use Better for a mortgage also receive a 1% rebate on the mortgage value, capped at $10,000, to cover closing costs. On an $800,000 mortgage that is an $8,000 rebate, partially offsetting the rate premium.

Why Fannie Mae Is the Key Piece

Every previous crypto-backed mortgage product has been a niche wealth management offering, high minimums, high rates, no secondary market. What makes this different is Fannie Mae. Fannie Mae is the Federal National Mortgage Association, a government-sponsored enterprise that purchases and guarantees mortgages from lenders, creating liquidity for the entire US housing market. It sets the conforming loan standards that govern roughly half of all US mortgages.

By structuring the Better/Coinbase product as a conforming Fannie Mae loan, the mortgage carries the same protections, the same secondary market access, and the same interest rate environment as any conventional mortgage. It is not a specialty product with a specialist rate sheet. It is a standard mortgage with a non-standard collateral structure for the down payment. That distinction is everything.

What This Means for the $12 Trillion US Housing Market

The immediate market impact is modest. One product from one originator does not move a $12 trillion market. But the structural signal is significant in three ways.

First, it unlocks suppressed demand. The 41% of families who cannot buy homes due to the down payment barrier are not all cash-poor. Many are asset-rich in crypto, equities, or other non-liquid forms. The Bitcoin mortgage is the first product that treats crypto wealth as a legitimate input into the housing finance system at the conforming loan level. If it succeeds, it creates a template for equity-backed, stock-backed, and other asset-backed conforming structures to follow.

Second, it changes the relationship between crypto and real estate. Bitcoin has been treated as a speculative asset, separate from and sometimes in competition with real estate as a wealth-building vehicle. The token-backed mortgage begins to integrate the two. Bitcoin becomes not a substitute for real estate wealth but a pathway into it.

Third, it reframes the down payment conversation nationally. The 7-year wait to save a down payment has been presented as a fixed structural reality. This product suggests it is a structural choice, one that can be redesigned as the collateral landscape evolves. If Fannie Mae accepts Bitcoin collateral today, the question becomes what other illiquid assets it might accept tomorrow.

Frequently Asked Questions